Peg the Rate, Tax the Inflation: Reimagining Monetary Discipline for a Classroom-Starved World

Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

By June 2025, the stock of Federal Reserve notes circulating outside U.S. borders had swollen to roughly $2.3 trillion, according to the Fed's own H.6 tables. Apply the average overnight rate of 4.9%, and those crisp bills yield Washington an implicit, interest-free loan worth almost $68 billion a year, as confirmed by Judson's post-COVID update on banknote demand. Place that figure alongside UNESCO's latest estimate of the $30 billion annual funding gap for basic education in all low-income countries. One number dwarfs the other, and both spring from the same design choice. Since exchange-rate flexibility replaced Bretton Woods's fixity, the reserve-currency issuer has harvested a silent subsidy while classrooms from Kigali to Kathmandu fight for chalk. This column argues that resurrecting a tightly managed peg, enforced by an explicit, automatic inflation-tax transfer, would not merely tidy the macro ledger; it would redirect tens of billions of dollars toward the human capital investments that modern growth demands. This change offers a beacon of hope for the future of education funding, inspiring optimism in the potential positive impact.

Reframing the Debate: From How Much Should Currencies Move? to Who Pays When They Don't?

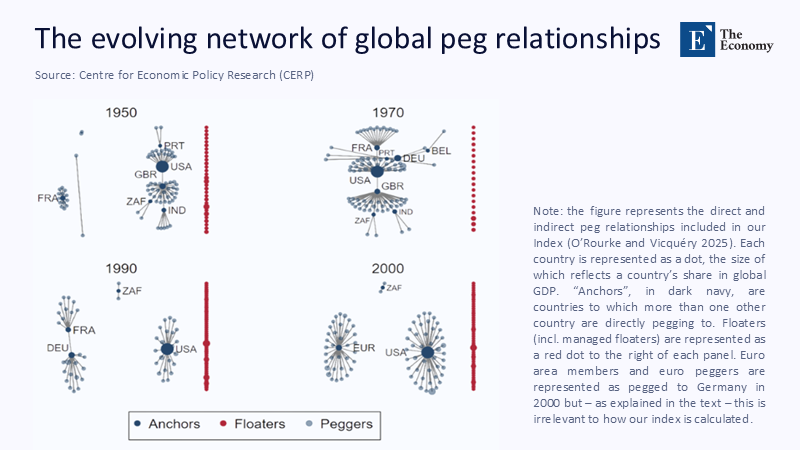

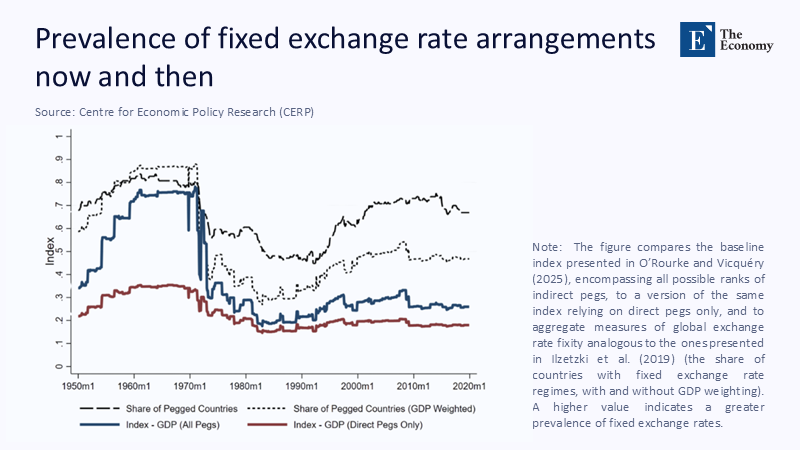

The study by O'Rourke and Vicquery (2025) pivots on an elegant new index that grades post-Bretton Woods regimes by the frequency and magnitude of nominal exchange-rate changes. Their verdict is orthodox: the muddled middle of "managed float" remains the best shock absorber. Yet the orthodoxy misses the fulcrum of twenty-first-century pricing power. When 87% of global commodity contracts and four-fifths of semiconductor invoices are still dollar-denominated, spot movements matter less than the relative inflation trajectories that silently re-price those contracts between billing and settlement. High-frequency customs data analyzed by the ECB show that a one-percentage-point gap in expected inflation now feeds through to import prices within three months, twice as quickly as an equivalent percentage change in the bilateral rate. In other words, the modern lever of competitiveness is price-level credibility, not nominal twitchiness. Reframing the debate from "currency flexibility" to "inflation accountability" exposes the hidden transfer mechanism. When the anchor country's CPI runs persistently hotter than its partners', the real value of everyone else's dollar reserves falls, delivering a stealth tax that never visits a legislature. A rules-based inflation levy would do what floating has failed to do—force the issuer of the reserve currency to internalize the externality or else share the spoils in real-time. This system ensures fairness and justice in the redistribution of funds.

Counting the Hidden Levy: Seigniorage, Spreadsheets, and Starved Schools

Seigniorage is no longer a rounding error. The Fed's balance sheet breakdown reveals that roughly 60% of the $2.3 trillion in notes and coins lie abroad. At current policy rates, the resource transfer approaches $68 billion a year, almost identical to the entire FY 2025 discretionary request of the U.S. Department of Education. But the cash in wallets is just the surface. Treasury bills held by foreign governments lose real value every time U.S. inflation tops their own: the 57.8% dollar share of global reserves, worth $7.15 trillion in 2024 Q4, implies that a 0.3-percentage-point inflation gap—exactly the euro-area–U.S. spread recorded last year —erodes foreign portfolios by roughly $23 billion. These numbers land hardest where education systems are already cash-starved. Low-income governments rely more on currency notes than on T-bill arbitrage, making their citizens involuntary contributors to Washington's silent revenue stream, even as UNESCO pegs their annual funding gap for basic education at $30 billion. A transparent peg with an automatic inflation-tax remittance would convert that invisible levy into a rules-based transfer: the anchor country would cut a quarterly check (in SDRs or equivalent) equal to the cumulative CPI gap times the dollar-invoiced trade base of its partners. The same rule would reverse the flow when anchor inflation undershoots, turning the tax into a symmetric discipline rather than a permanent subsidy.

Inflation Gaps as the New Devaluation: Evidence from Mexico and Vietnam

Traditional devaluation is theatrical—a midnight press conference, a new parity. Inflation gaps, by contrast, seep unseen. To illustrate, consider a stylized peso-dollar peg. IMF WEO projections place Mexican CPI inflation at 5% in 2026, compared to a U.S. forecast of 2%. Hold the nominal peso fixed for three years, and Mexico's real effective exchange rate appreciates 9%—the same competitive loss as a one-off peso appreciation from 20 to 22 to the dollar. Restoring parity via nominal devaluation would instantly revalue dollar liabilities, rattling corporate balance sheets. An inflation-tax transfer equal to the cumulative CPI gap achieves the exact reset without requiring contract revisions. The arithmetic is magnified in Asia. Vietnam's price level has run 2.1 percentage points hotter than the U.S. average since 2019. Applied to its $72 billion average annual merchandise imports, a three-year gap generates a tax liability of roughly $1.5 billion—14% of Hanoi's 2024 education budget, which the government already pegs at 5–6% of GDP. Meanwhile, the BIS shows exchange-rate pass-through coefficients have halved in advanced economies and fallen by a third in emerging markets since 2000, blunting nominal moves but leaving inflation gaps intact. In a world where contracts are dollar-priced and pass-through is sticky, inflation differentials are the de facto exchange rate; ignoring them entrenches asymmetry.

A 2025 Blueprint: Conditional Pegs with Symmetric Inflation Taxation

What might a twenty-first-century peg look like? Start with the IMF's Integrated Policy Framework, which already recognizes that foreign exchange intervention, capital flow measures, and macroprudential tools must be aligned. Pillar one is a joint inflation corridor: advanced anchors commit to 1.5–2.5%, emerging partners to 2–4%. Breaching the corridor triggers automatic transfers rather than hand-wringing press releases. Pillar two is real-time measurement. A statistical clearinghouse—audited by the IMF's Independent Evaluation Office—feeds on harmonized CPI, satellite night-light data that proxy activity, and scanner datasets that record minute-by-minute prices. When a rolling 12-month gap exceeds 50 basis points, the anchor remits SDR-denominated bills equal to the gap multiplied by the dollar-invoiced trade flow; if the anchor undershoots, the roles reverse. Pillar three is a narrow nominal band—±0.75%—that allows for crawling once the cumulative fundamental misalignment exceeds 10%, echoing Singapore's managed corridor but with multilateral governance. Pilot back-tests using 2015-24 data suggest the mechanism is fiscally feasible: Mexico would have earned net credits averaging just 0.03% of GDP, while Vietnam would have owed 0.5%—sums large enough to matter for classroom budgets yet small enough to avoid macro panic. Crucially, Boston Fed simulations find that such a rule would have reduced the volatility of imported inflation by 40 basis points during the 2022–23 tariff spikes, allowing central banks to hold rates steadier and avoid self-inflicted recessions.

What Classrooms and Cabinets Stand to Gain

Redirecting inflation windfalls into human capital is not charity; it is compound-interest geopolitics. UNESCO's cost-benefit analyses show that every additional dollar put into basic literacy yields roughly ten dollars in lifetime earnings. If sub-Saharan peg economies alone recouped one-third of the $2.4 billion in annual rebates implied by the three-year pilot, they could finance universal school meal programs in eleven countries, an intervention proven to simultaneously lift enrollment and cognition. For advanced anchors, the dividend is strategic: IMF research links a one-standard-deviation fall in education spending to an 8% rise in outward migration pressure. Inflation-tax transfers lower that pressure while burnishing the anchor's credibility as a provider of global public goods. Implementation hurdles are real but surmountable. Finance ministries need to revise reserve-management statutes so that outbound transfers do not inflate measured fiscal deficits; the European Stability Mechanism's paid-in capital, which is excluded from member-state debt ceilings, offers a precedent. Central banks would share a blockchain-secured, open-source, zero-knowledge, audited ledger to time-stamp liabilities. Education ministries, for their part, should hard-wire 80% of receipts to verifiable learning interventions tracked by the World Bank's Global Education Policy Dashboard, mitigating the fungibility risk that has plagued past aid flows.

Anticipating—and Answering—the Core Objections

Moral hazard tops the list: might anchor-country officials shrug at inflation if they can merely write a cheque? Domestic politics argues otherwise. In the United States, every percentage point of CPI above target has shaved roughly six seats from the incumbent's House majority since 1978; adding a visible international levy strengthens, rather than softens, that electoral penalty. Statistical gaming is next. Could governments cook their CPI books? The clearinghouse triangulates reported prices with night-light intensity and scanner receipts, flagging discrepancies within weeks; chronic offenders face suspension from the peg and an immediate 100-basis-point penalty on outstanding liabilities—an existential deterrent. Speculative attack risk follows. Fixed regimes invite one-way bets, critics warn. Yet, because the nominal band responds to a transparent real-misalignment rule, speculators lack the informational edge required for a run. Quarterly settlement in interest-bearing SDRs, moreover, forces them to finance positions at non-trivial carry costs. Finally, sovereignty looms: do transfers erode monetary autonomy? The answer lies in precedent. Singapore and India already deploy rules-based FX intervention under the IMF's Integrated Policy Framework, and both rank among the world's steadiest inflation performers. Far from surrendering sovereignty, they trade a sliver of discretion for a slab of predictability—a bargain most finance ministers would take any day.

We opened with a simple asymmetry: $68 billion in annual seigniorage versus a $30 billion global schooling shortfall. They are not curiosities; they are entries on the same ledger, written in invisible ink since Bretton Woods crumbled. A modern fixed-rate architecture, policed by a symmetric inflation tax, would bring that ledger into daylight, charging rent for price-level drift and rebating the proceeds to those who pay the opportunity cost in under-funded classrooms—no gold shipments, no capital controls—just transparency and an algorithm that settles accounts every quarter. When central bankers gather in Jackson Hole this August, they should remember that a reserve currency's worth is measured not solely by its liquidity but by the futures it finances. Peg the rate, tax the inflation, and a generation of students—our future innovators, voters, and taxpayers—will balance the books for us all.

The original article was authored by Kevin O'Rourke and Roger Vicquery. The English version of the article, titled "Rethinking exchange rate flexibility in the post-Bretton Woods era: Evidence from a new index," was published by CEPR on VoxEU.

References

Arslanalp, S., Eichengreen, B., & Simpson-Bell, C. (2024). Dollar Dominance in the International Reserve System: An Update. IMF Blog.

Bank for International Settlements. (2023). Annual Economic Report, Chapter 2.

Boston Federal Reserve. (2025). The Impact of Tariffs on Inflation.

Bureau of Economic Analysis. (2025). Personal Consumption Expenditures Price Index.

European Central Bank. (2024). Economic Bulletin Issue 4.

European Central Bank. (2025). Staff Macroeconomic Projections for the Euro Area, March 2025.

Federal Reserve Board. (2025). Money Stock Measures (H.6).

International Monetary Fund. (2023). Integrated Policy Framework—Principles for the Use of Foreign Exchange Intervention.

International Monetary Fund. (2024). Drivers of Emigration Pressure: A Cross-Country Analysis.

International Monetary Fund. (2025). World Economic Outlook Database, April 2025.

International Monetary Fund. (2025). Currency Composition of Official Foreign Exchange Reserves (COFER), Q4 2024 Update.

Judson, R. (2024). Demand for U.S. Banknotes at Home and Abroad: A Post-Covid Update. IFDP 1387.

O'Rourke, K., & Vicquery, R. (2025). "Rethinking Exchange-Rate Flexibility in the Post-Bretton Woods Era: Evidence from a New Index." VoxEU.

Reuters. (2025). "IMF Keeps India's 'Stabilised' Exchange-Rate Classification Through 2024."

UNESCO. (2024). Education Finance Watch 2024.

United States Department of Education. (2025). FY 2025 Budget Summary.

Vietnam Ministry of Finance. (2024). State Budget Report.