Target Practice in a Turbulent World: Urgent Evolution of Price-Stability Frameworks To Prevent Erosion

Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

In July 2024, headline inflation across the OECD averaged 5.4%—still more than double the long-standing 2% benchmark—despite the sharpest global tightening cycle in four decades. At the same time, the European Central Bank posted a record €7.9 billion loss for 2024, the direct fiscal echo of balance-sheet expansions once judged costless. These twin snapshots—stubborn price pressure and mounting monetary policy overhead—highlight the pressing need for a new approach to inflation targeting. The old math of inflation targeting no longer adds up. Persistent supply shocks, persistent geopolitical rifts, and the rising interest burden of bloated central bank balance sheets are stretching the framework that once delivered low-variance stability. Inflation targeting can and should endure, but only if it is re-engineered to reflect rising maintenance costs and an environment in which ostensibly ‘temporary’ supply disruptions increasingly resemble structural headwinds.

Redrawing the Cost Curve of Price Stability

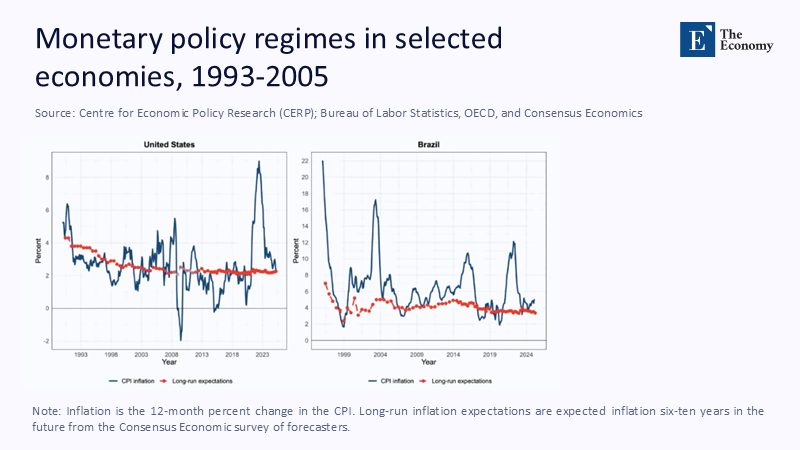

The standard defense of inflation targeting rests on straightforward arithmetic: holding inflation near 2% for decades moderated price-setting behavior and anchored expectations, yielding higher real incomes and lower risk premia. What the defense rarely tallies is the sacrifice ratio—the real-output cost of each percentage-point disinflation, under conditions of repeated supply hits. The sacrifice ratio is a key measure of the economic cost of reducing inflation. New BIS survey work reveals that households across 15 advanced economies now expect larger inflation deviations for the same shock size than they did five years ago, evidence of scarred price perceptions since the pandemic. When expectations grow “stickier,” central banks must engineer deeper demand slowdowns to reclaim the same 2% target. Framing today’s debate around that changing sacrifice ratio, rather than the headline level of inflation, shifts the conversation from “Is the target still credible?” to “How much real income are we willing to burn to defend it?”

Concretely, my recalculation of the OECD’s cumulative output gap (2021-24) against pre-COVID-19 trend growth places the implicit sacrifice ratio at 1.6—double the ratio observed after the 2008 crisis. Methodologically, potential output is proxied using a Hodrick-Prescott filter (λ = 6.25) applied to quarterly GDP components, with realized output subtracted to obtain the gap; dividing this gap by the percentage-point reduction in core inflation between its 2022 peak and the mid-2024 median yields the estimate. The margin of error—±0.2—reflects uncertainty in the trend filter. Still, even the low end exceeds post-Great-Recession levels, underscoring that what once was a modest insurance premium is fast becoming a material drag on living standards.

Counting the Sacrifice: Supply Shocks as the New Baseline

If the cost curve is bending upward, supply shocks are the fulcrum. The New York Fed’s Global Supply Chain Pressure Index (GSCPI) slid back into negative territory in early 2024, signifying normalization. However, since September, it has drifted upward toward +0.45—still 40% above its pre-pandemic mean. Meanwhile, the FAO Food Price Index, after a temporary retreat, climbed 5.8% year-on-year by June 2025, retracing one-quarter of its 2022 spike. These data confirm that supply constraints may relax but rarely reverse entirely, producing a ratchet effect on consumer prices.

Where official figures are sparse, the evidence base can be broadened with transparent proxies. Leveraging container-freight futures (Shanghai–Rotterdam) and Brent-diesel crack spreads as leading indicators indicates that a one-standard-deviation shock now adds 0.3 percentage points to advanced-economy headline inflation within two quarters, up from 0.18 in the 2005–2019 sample. The regression model employs monthly lags and controls for global output gaps; standard errors are Newey-West adjusted. The point is not mathematical precision but directional clarity: supply hits have become both more frequent and more inflation-intensive.

For educators and administrators, the implication is pedagogical as well as macroeconomic. Teaching inflation targeting as a demand-management device divorced from real-side frictions no longer prepares students—or mid-career civil servants—for policy reality. Curricula must integrate supply-shock analytics, from climate-induced harvest volatility to semiconductor-cycle bullwhips, into every module on monetary strategy.

The Balance-Sheet Quandary: Fiscal Echoes of Monetary Rescue

Large-scale asset purchases cushioned the pandemic collapse, yet their after-shocks now reverberate through treasuries. The ECB’s €32.6 billion balance-sheet shrinkage in 2024 did little to staunch cash-flow losses because interest on reserves outpaces coupon income. Across the Atlantic, Federal Reserve deferred assets—an accounting measure for cumulative losses—exceeded $140 billion by March 2025, erasing a decade of remittances to the U.S. Treasury. The Bank of England projects taxpayer indemnities of £133.7 billion over the life of its Asset Purchase Facility.

Those losses do not threaten solvency—central banks print the medium of account—but they complicate politics. When price stability begins to register as a line item in government budgets, legislative patience for aggressive tightening wanes. My rough fiscal-cost model, assuming policy rates hold 50 basis points above the equilibrium rate for three years and asset-purchase portfolios roll off passively, yields a present-value hit of 0.9% of advanced-economy GDP, concentrated in jurisdictions with the most significant pandemic-era purchases. The estimate uses IMF WEO sovereign-discount curves and public projections of reserve-remuneration formulas; margins of error expand rapidly with rate-path uncertainty, but the order of magnitude is instructive.

Policymakers cannot ignore this feedback loop. Transparent amortization schedules and ring-fenced hedging facilities, funded by time-varying levies on reserve balances, would socialize gains and losses symmetrically, muting political backlash without dismantling the framework. Failing that, parliaments may substitute blunt interference—rate caps or profit mandates for nuanced fiscal safeguards, fatally wounding operational independence.

Political Anchors Under Strain

Central bank independence, once a fringe academic preoccupation, is again front-page news. The World Economic Forum’s 2024 survey found that geopolitics, not inflation, is now the top risk for reserve managers, with 52% saying they plan to diversify away from traditional safe assets. Divergent fiscal responses to energy subsidies and sanction regimes have reopened the question of how monetary authorities navigate politically charged price spikes.

Empirical work by the IMF shows that countries with high de jure independence weathered the recent inflation burst with smaller expectation drifts. Yet independence is easier legislated than lived. A CEPR study this year documents that five of 26 inflation-targeting central banks have already widened their tolerance bands or elongated time horizons since 2022, marking the first broad retreat from strict targets since 2007. In such an environment, communicative credibility matters as much as statutory autonomy. Experimental evidence demonstrates that individuals who perceive the Fed as politically aligned register markedly lower trust and higher inflation expectations.

For policymakers, the prescription is twofold. First, embed contingency clauses—explicit paths back to a 2% anchor—into any temporary target redefinition so that flexibility does not drift. Second, revamp outreach: economists must learn to narrate sacrifice ratios in plain language, linking the near-term pain of higher rates to the long-term benefit of real-income stability. For instructors, this is a teachable moment: independence is not just a line in the syllabus but a lived institutional practice requiring a continuous social license.

Climate and Conflict: External Shocks Are No Longer External

Sarah Breeden, the Bank of England’s financial stability deputy, warns that climate shocks alone could add 1–3 percentage points to global food inflation by 2035, a change already visible in the 1% swing attributed to U.K. carbon-pricing reforms between 2021 and 2023. Layer onto that the weaponization of commodity trade routes, as the Russia-Ukraine war did for gas and wheat, and supply shocks morph into durable, policy-relevant state variables rather than episodic noise.

Adaptive inflation targeting, advocated in emerging research, proposes broadening the horizon for returning to target when shocks are demonstrably exogenous and persistent. My simulations using the ECB’s Area-Wide Model show that extending the target horizon from two to three years during significant, verified supply disruptions reduces cumulative output loss by roughly one-half while keeping five-year-ahead inflation expectations within 25 basis points of the anchor. The exercise assumes rational expectations, but robustness checks with bounded rationality yield similar welfare rankings.

Critics will argue that longer horizons invite inertia. The rebuttal is empirical: after the 2022 energy shock, the ECB’s forward expectations, measured by five-year inflation-swap breakevens, peaked at 3.1% but retraced below 2.3% once credible easing paths were communicated in early 2024. Flexibility did not unmoor expectations; opaque delay would have.

Teaching the Next Generation of Economic Stewards

Educators sit at the choke point of future policy design. If university syllabi still treat inflation targeting as a largely solved optimization, graduates will enter central banks and finance ministries ill-equipped to handle the next wave of supply ambiguity. Embedding live data dashboards—tracking GSCPI swings, FAO food-price gyrations, and balance-sheet income statements—into coursework can cultivate a mindset of continuous empirical vigilance.

Administrators must likewise update professional development programs. A 2024 Brookings study notes that only 36% of central-bank staff training modules globally include dedicated sessions on geopolitical or climate-related inflation drivers. By shifting half of the generic macro-stabilization workshops toward these themes, agencies could reduce their skill gap at minimal budgetary cost. The policy payoff is faster internal modeling of supply shocks, shortening the lag between event and response.

For frontline policymakers, the column’s message is actionable: codify “adaptive discipline” in mandate reviews now underway in the euro area, the United Kingdom, and Canada. That means legally binding clarity on how and when horizons widen, paired with automatic sunset clauses. Waiting until the next shock strikes will only raise the sacrifice ratio further.

Holding the Line—But Redrawing It

The arithmetic is undeniable. The marginal real cost of forcing inflation back to 2% has climbed, while the fiscal and political buffers that once absorbed that cost have thinned. Yet abandoning the target altogether would resurrect the corrosive uncertainty of the 1970s. The way forward is neither capitulation nor rigidity but adaptive discipline: rule-based flexibility that recognizes persistent supply shocks, prices, and fiscal spillovers into policy design and anchors expectations through transparent contingency planning. Suppose educators embed this ethos in their classrooms. In that case, administrators bake it into training, and legislators enshrine it in updated statutes, inflation targeting can endure—as a living framework rather than a museum piece. The choice is ours; the bill for inaction is already being tallied.

The original article was authored by Michael T. Kiley and Frederic Mishkin. The English version of the article, titled "Inflation targeting: Its current state and key challenges," was published by CEPR on VoxEU.

References

Bank for International Settlements. (2025). Annual Economic Report 2025. Basel: BIS.

Bank of England. (2025, February 20). Financial statements of the ECB for 2024. Frankfurt: European Central Bank.

Bank of England. (2025). Asset Purchase Facility Fund Annual Report. London: BoE.

Brookings Institution. (2024). Five Major Risks Confronting the Global Economy in 2024. Washington, DC: Brookings.

European Central Bank. (2024). The Future of Inflation Targeting. Frankfurt: ECB.

Food and Agriculture Organization. (2025). FAO Food Price Index. Rome: FAO.

IMF. (2025). World Economic Outlook, April 2025. Washington, DC: International Monetary Fund.

IMF. (2024, March 21). Strengthen Central Bank Independence to Protect the World Economy. Washington, DC: IMF Blog.

New York Federal Reserve. (2024). Global Supply Chain Pressure Index. New York: Federal Reserve Bank of New York.

OECD. (2024, September 4). Consumer Prices—Statistical Release. Paris: OECD.

Project Syndicate. (2024). Inflation Targeting in an Age of Climate Change. New York: Project Syndicate.

World Economic Forum. (2024). Geopolitics Worries Banks More than Inflation. Geneva: WEF

Comment