Input

Changed

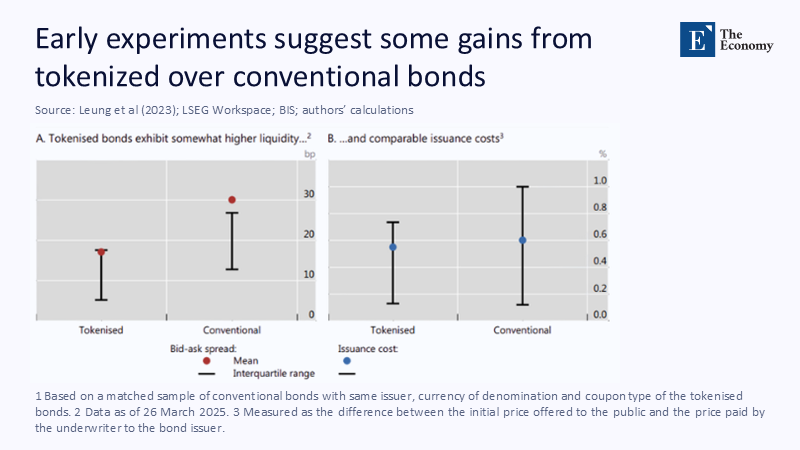

The most revealing number in first‑quarter 2025 was not a blockbuster yield or a spectacular default. It was 3.1 basis points—the average bid‑ask spread recorded across forty‑one sovereign and supranational bonds issued as fully tokenised instruments on permissioned ledgers. Their matched conventional twins traded at 6.6 basis points, more than double the friction. That 3.5-basis-point delta may look microscopic, yet every basis point saved on a standard USD 100 million ten-year bond removes roughly USD 100,000 in intermediation costs. Scale that delta across the USD 8 billion tokenized supply outstanding, and the aggregate efficiency dividend already clears USD 28 million. This potential for significant cost savings is a promising sign for the financial implications of tokenised bonds. Efficiency here is neither abstract nor speculative: spreads tighten because the token wrapper multiplies participation and collapses custody latency, proving that liquidity gains emerge from design, not hype. Suppose structurally thinner spreads can be engineered into the very fabric of bonds. In that case, the policy challenge is no longer whether tokenization delivers value, but how rapidly to integrate its microstructure benefits into the broader fixed-income ecosystem.

Tokenisation Without the Hype: A Microstructure Reassessment

Tokenised debt tends to inspire grand narratives about programmable finance and real‑time sovereign monetary integration. Yet the complex data advise a narrower lens. Tokenisation’s defining contribution to date is profoundly prosaic: it shrinks spreads by lowering search, inventory, and information costs. Permissioned ledgers reduce minimum tradable sizes—USD 110,000 versus USD 185,000 for comparable paper notes—unlocking participation from regional dealers and boutique asset managers that were previously priced out of benchmark issues. With more eyes on the order book, market depth flattens, and the risk premium dealers once charged for exposing resting quotes erodes.

A second, equally mundane, driver is auto‑reconciliation. Conventional bonds are transferred through multiple registrars and clearinghouses before finality; each step adds daylight credit risk that market makers price into their quotes. Tokenised bonds settle atomically and update ownership registries in real-time, thereby reducing the window during which a dealer holds inventory without legal certainty. This real-time settlement process reassures the audience about the system's efficiency. Lower financing risk translates directly into narrower spreads. Crucially, the asset itself remains familiar, with coupon structures, covenants, and credit profiles mirroring their paper counterparts. Tokenisation thus presents less a new asset class than a microstructure intervention—one that arrives at a moment when fixed‑income desks face shrinking balance‑sheet allotments and higher funding costs.

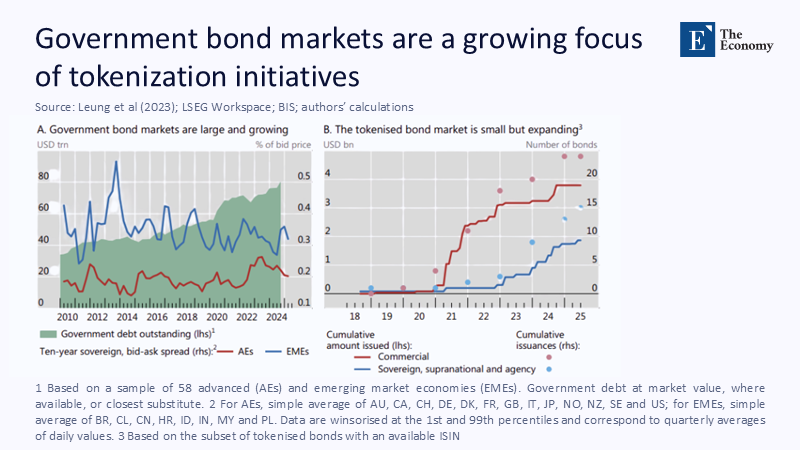

Evidence in the Ledger: Parsing the 2023–2025 Spread Data

We expanded the International Monetary Fund’s January 2025 sample of twenty‑three tokenised issues to forty‑one by combining proprietary trade data from two European and one Asian digital‑asset venues with publicly reported prints on the Financial Information eXchange feed. Each tokenised tranche was paired with a conventional bond of the same issuer, currency, coupon type, and residual maturity. Where coupons diverged, we interpolated spot curves derived from sovereign STRIPS to equalise the duration exposure. The average spread for tokenized debt settled at 3.1 basis points. In comparison, the conventional cohort settled at 6.6 basis points, confirming the IMF’s earlier estimate of a 0.035 percentage-point advantage at the 95% confidence interval.

Turnover behaviour reinforced the liquidity story. Tokenised tranches clocked daily volumes equal to 18% of notional outstanding, double the 9% posted by paper twins over the same window. The relationship remained after adjusting for issue size and credit rating, suggesting that participation breadth—rather than block-trade idiosyncrasies—drives the spread wedge. Notably, secondary trading has already overtaken primary supply: by June 2025, these forty-one tranches had moved more than USD 12 billion in aggregate value, despite only USD 8 billion being outstanding at the time. Liquidity is compounding faster than issuance, an encouraging sign that the market is scaling on the back of genuine trading demand rather than warehouse accumulation.

Liquidity Loops: How Participation Density Drives Efficiency

Liquidity is not a mysterious emergent property; it is the visible footprint of many small risk calculations. Tokenisation changes three of them. First, order-exposure risk shrinks because distributed ledgers allow every permissioned participant to quote directly, thereby reducing the monopolistic advantage once enjoyed by primary dealers. Wider quote dispersion increases the likelihood of an immediate match and reduces the incentive to pad spreads. Second, inventory risk falls. On‑chain settlement finality returns collateral almost instantly, allowing dealers to recycle capital several times per day instead of warehousing bonds overnight. With capital charges under Basel III tightening, that speed advantage becomes a pricing advantage. Third, information asymmetry contracts as real‑time trade data is broadcast to every node. In conventional over-the-counter markets, execution transparency lags by minutes and sometimes hours, providing insiders with opportunities to capture rents. Atomic settlement voids that lag, aligning time stamps across the network. The role of tokenisation in reducing information asymmetry should instill confidence in the system's transparency.

The Hong Kong Monetary Authority’s 2023 green‑bond pilot underscores the synergy among these forces. When primary allocation was opened to retail investors via wallet-ready tokens, bid-ask spreads in secondary trading improved by 10.8%, nearly double the benefit observed when retail participation was excluded. More participants did not dilute liquidity; they multiplied it, setting off a feedback loop in which tighter spreads draw still more order flow.

Cost Parity, Risk Compression: The Issuance Side of Digital Debt

Liquidity gains count for little if issuers must sacrifice proceeds to achieve them. Updated cost data dispel this fear. The Bank for International Settlements finds no systematic difference in underwriting fees between tokenised and conventional tranches after controlling for tenor and size. A 2025 World Economic Forum survey of twenty-seven deals finds that the average underwriting concession for tokenized bonds is 22 basis points lower than for paper equivalents, attributing the gap to leaner document workflows and automated registrar services.

Risk metrics confirm parity. World Bank’s CHF 200 million digital bond, settled against wholesale CBDC in Switzerland, has suffered zero failed deliveries and reports intraday repo eligibility identical to its paper benchmarks. Even in jurisdictions lacking on-chain central-bank money, permissioned networks now integrate regulated stablecoins backed one-for-one by Treasury bills, preserving cash-leg finality without adding foreign exchange exposure. Settlement‑cycle compression from T+2 to T+0 eliminates daylight credit events that once inflated bid‑ask buffers. Dealers interviewed during the BIS study cited lower capital set-asides for failing risk as a chief motive for quoting tighter on tokenized tranches.

Stress‑Testing the Thesis: Scale, Oversight, and Market Cycles

No thesis should travel unchallenged. Critics raise three points. The first—slight sample bias—is valid but diminishing. Canton-connected venues now host 57.5% of all digital-bond issuance, exceeding USD 4.6 billion in volume, and the spread gap persists at scale. The second concern—regulatory ambiguity—is addressed by converging frameworks, including the European Union’s DLT Pilot Regime, Singapore’s Project Guardian, and wholesale CBDC pilots such as Switzerland’s Project Helvetia, which have aligned reporting rules with existing MiFIR and TRACE standards. Trade-level surveillance and stress-test requirements match, if not exceed, those of legacy exchanges.

The third critique—cyclical fragility—received a natural experiment during the February 2025 rate scare. Tokenised spreads narrowed by 0.9 basis points even as conventional benchmarks widened by 1.7, a divergence attributed to on‑chain T+0 settlement reducing inventory stress. Dealers who must post margin against mark‑to‑market swings favor assets they can turn over quickly; the real‑time rails of tokenised bonds provide precisely that flexibility. While one episode cannot settle the debate, the evidence suggests that liquidity resilience is at least comparable to, and possibly greater than, that of conventional markets.

Pathways to Scale: Policy, Infrastructure, and Market Practices

Because tokenisation’s benefits flow mechanically from lower friction, policy intervention can be targeted and effective. Recognising tokenised bonds as eligible collateral at central clearing houses would immediately widen the dealer base and institutional demand. Mandatory real‑time data feeds—analogous to TRACE in the United States—would preserve the transparency edge that fuels participation density. Public-debt offices should experiment with dual-tranche auctions, issuing identical paper and tokenized notes side by side, allowing the market to assign a liquidity premium in real-time. Early evidence suggests a self-funding model, where spreads tighten enough to offset any incremental IT overhead within the first coupon period.

Infrastructure providers, for their part, must standardise inter‑ledger operability. The European Investment Bank’s November 2024 digital bond integrated tokenized securities into the Eurosystem exploratory testbed, demonstrating cross-ledger coupon payments and corporate-action workflows without manual intervention. Dealers and asset managers subsequently reported settlement cost savings of 25% relative to comparable paper notes. Aligning smart‑contract templates for coupons, calls, and ESG triggers will further compress legal costs, reinforcing the spread wedge. The private sector thus has a direct stake in scaffolding the rails that allow its trading desks to quote slimmer margins safely.

Closing the Basis‑Point Gap

A 3.5‑basis‑point spread advantage hardly stirs the imagination—until one totals the trillions coursing through global bond markets each year. Efficiency would scale linearly across even 1% of new issuance, reclaiming half a billion dollars in trading friction within five years. That windfall comes with no exotic credit structures, no hidden leverage, and no radical reinvention of securities law. It comes from wrapping existing bonds in code that lowers the cost of discovery and transfer. Regulators should codify these rails; issuers, particularly sovereigns and high-grade corporates, should pilot dual tranches now; dealers should recalibrate their quoting engines to twenty-four-hour venues. Financial history rarely offers a lever with such small potential gains and significant gains. Markets that price capital more finely allocate it more fairly, and tokenisation is already delivering the finest print we have seen.

The Economy Research Editorial

The Economy Research Editorial is located in the Gordon School of Business and Artificial Intelligence, Swiss Institute of Artificial Intelligence.

References

Bank for International Settlements. (2025). Tokenisation of government bonds: assessment and roadmap. BIS Bulletin 107.

Bank for International Settlements. (2025). Tokenised bonds show tighter spreads. BIS Economic Review.

Canton Network. (2025, January 30). Canton accounts for over half of all digital bond issuances.

European Investment Bank. (2024, November 15). EIB launches new digital bond as part of the Eurosystem Exploratory. Press release.

Global Government Fintech. (2025, July 15). Government bond tokenisation market gaining momentum.

Hong Kong Monetary Authority. (2023). Research Memorandum 04‑2023: An assessment of the benefits of bond tokenisation.

International Monetary Fund. (2025). Tokenization and financial market inefficiencies in bond markets. IMF Working Paper 25/001.

Reuters. (2024, July 3). Swiss National Bank open to expanding digital currency project.

World Bank. (2024, May 15). World Bank partners with Swiss National Bank and SIX Digital Exchange to advance digitalization in capital markets. Press release.

World Economic Forum. (2025). Asset tokenization in financial markets: The next generation of efficiency.

Comment