Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

Policy theatrics end where arithmetic begins, and the numbers now say the show is costing the audience.

A Shockwave Measured in Trillions

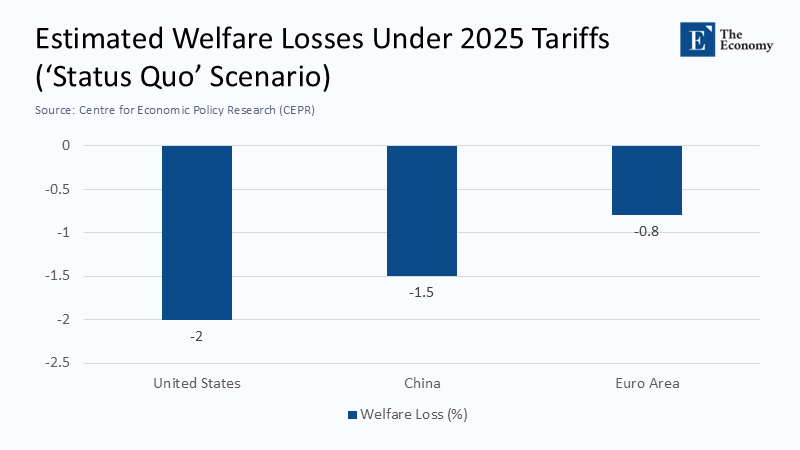

The CEPR simulation of the 2025 tariff package shows that the United States endures a welfare decline near ‑2 % under the still‑cushioned “status quo” path. China absorbs roughly ‑1.5 %, while the euro area loses less than ‑0.8 %.

That 2 % headline may sound abstract until converted into dollars: on a $28 trillion economy, the hit equals about $560 billion yearly, more than the combined annual budgets of the Departments of Education, Energy, and State. By contrast, the same percentage loss in China disperses through a far wider web of global linkages, muting domestic visibility.

From 3 % to 30 %: Explaining the Multiplier Effect

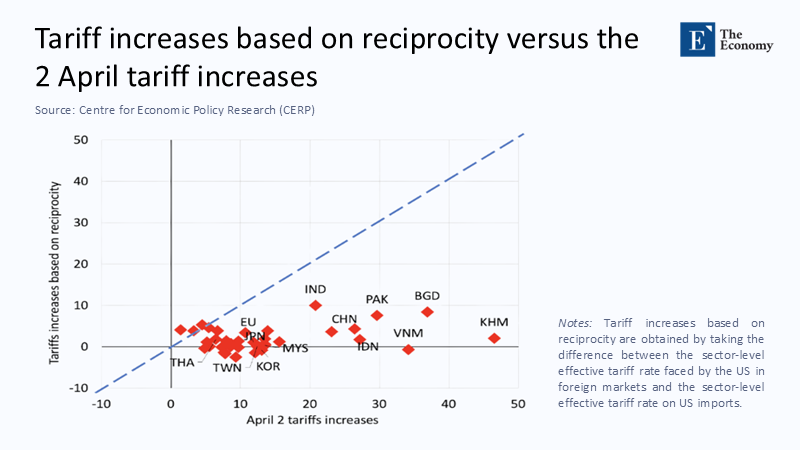

Before January, the average US tariff hovered near 3 %, pushing that rate to 30 %. Critically, as the Figure below shows, the burden is not even allocated according to reciprocity.. Within four months, an overlapping lattice of Section 301 and national security duties pushed that rate close to 30 %, and should Washington lift the 90‑day respite in July, the effective rate would breach 38 %. This drastic increase in tariffs has a significant multiplier effect. For every dollar of tariffs imposed, the overall economic impact is much larger, leading to a substantial decline in welfare.

Tariffs do not merely tax final goods. Nearly half of the US manufacturing value derives from imported inputs. When the price of an automotive semiconductor or a machine‑tool spindle spikes, every assembly line downstream inherits the markup, compressing margins or upping sticker prices. The CEPR model counts this cascade: purely domestic production ticks up by a fraction, yet output tied to global value chains falls sharply so that aggregate gross output shrinks. The intuition is brutal: the United States gains a few assembly jobs while surrendering larger chunks of integrated activity.

The Household Arithmetic Behind Macro Headlines

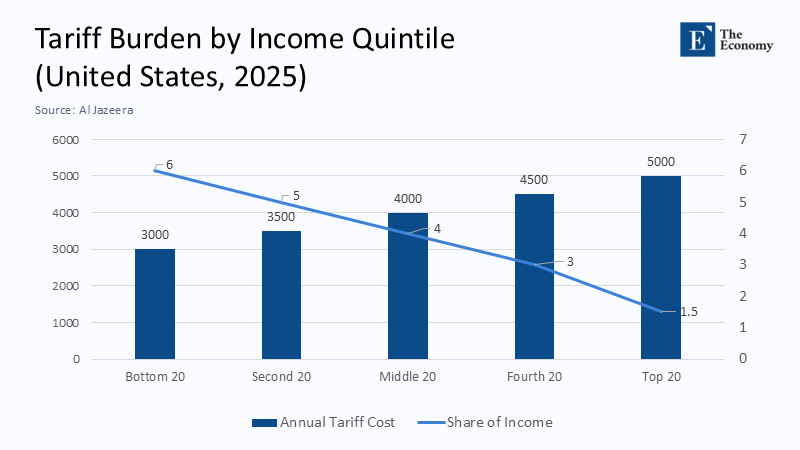

Al Jazeera’s round‑up of academic and private forecasters converges on a toll of roughly $4,000 per typical US household—an invisible tax equal to two months of grocery bills. The burden, however, is not evenly distributed.

The dual‑axis chart above shows that while top‑quintile households may pay $ 5,000, the cost represents barely 2 % of their disposable income. For bottom‑quintile families, a $ 3,000 hit swallows 6 % of after‑tax pay, crowding out rent, medical co‑pays, or a year of community college tuition.

What looks like an across‑the‑board “China tax” operates as a regressive levy. Because lower-income people spend a higher share on goods, the pass‑through into retail prices lands hardest on precisely the voters the policy purports to champion.

Indirect Exports and the Myth of Decoupling

CEPR’s value‑added tracing reveals that direct Chinese exports to the United States fell by $408 billion, yet indirect flows routed through third‑country hubs dropped only by $40 billion. This data dispels the myth of decoupling, which suggests that the US and China can sever their economic ties without significant consequences. In reality, more than half of the surviving content arrives via Mexico; another quarter passes through Vietnam or Korea, demonstrating global trade's complex and interconnected nature.

Supply chains, in other words, adapt faster than customs officers. The same Shenzhen‑designed microcontroller is diced and surface‑mounted in Guadalajara, then crosses the Rio Grande as NAFTA‑qualified. Policing such round trips demands forensic rules‑of‑origin audits that raise compliance costs for every importer—a Texas aerospace firm or an Ohio auto parts supplier. Instead of a steel wall, Washington has erected a toll gate whose price American producers must repeatedly pay.

Spillovers, Diversions, and the Waning of Leverage

Global trade volume contracts up to 8.5 % in the full‑retaliation path. Yet the pain is not symmetric. European firms find new openings in US consumer markets once Chinese electronics exit retail shelves. Japanese and Korean semiconductor giants gain share in server hardware. Some Latin American agribusinesses benefit from Beijing’s counter‑tariffs on US soy, corn, and pork.

Washington imagined leverage by framing tariffs as a bargaining chip. The data say otherwise: allies are hedging rather than lining up behind the United States. European finance ministries accelerate efforts to internationalize the euro in cross‑border settlements; ASEAN central banks pilot yuan‑linked swap lines to ensure against dollar liquidity shocks. A tool meant to intimidate adversaries now prods neutrals to dilute American monetary influence.

Dynamic Losses: Investment, Innovation, and the Real Option to Wait

Tariffs introduce a macro‑uncertainty premium. Firms confronted with volatile duty schedules and product‑specific licensing delays adopt a wait‑and‑see posture on capital expenditure. This 'real option to wait' refers to the strategic decision-making process where firms delay investment decisions amid uncertainty, such as fluctuating tariffs. According to the Federal Reserve’s macro model, each 10 % tariff shock raises the user cost of capital by roughly 30 basis points, magnified across a 30 % average duty, that kills borderline projects in electric‑vehicle batteries, solar‑glass rolling, and precision robotics—areas where the United States claims it wants strategic autonomy.

Moreover, some intangible losses never hit GDP tables. When Taiwanese chip fabricators choose Singapore for a new packaging plant rather than Arizona because contract terms require tariff‑proof back‑and‑forth of wafers, the capacity is not merely diverted; it becomes path‑dependent. Future modules that might have clustered in the Southwest now orbit the Straits of Malacca instead.

Why the Optics Outshone the Economics

A tariff can be justified under two defensible logics: protecting infant industries with diminishing cost curves or counteracting demonstrable unfair trade practices. The 2025 salvo fails both tests. Semiconductor fabrication, advanced textiles, and pharmaceutical precursors are capital‑intensive, not infant. Meanwhile, the tariffs blanket products irrespective of proven dumping or subsidy cases, diluting any legal argument at the WTO and inviting calibrated retaliation.

Crucially, the prudent sequencing of economic statecraft is a lesson we can all learn from. Resilience should precede coercion: first, subsidize redundant capacity, stockpile critical minerals, and build workforce pipelines; then, once strategic slack exists, tax the adversary’s exports. By firing the tariff gun first, policymakers drained fiscal resources and alienated suppliers whose cooperation is indispensable for dual‑use technology control.

The Opportunity Cost of Stubbornness

Consider the back‑of‑the‑envelope alternative. Redirecting half of the projected $560 billion annual welfare loss toward supply‑chain grants and advanced manufacturing tax credits could finance a decade of factory build‑out equal to three more TSMC‑Arizona fabs yearly. Moreover, a minor but smarter carbon border adjustment, aligned with European CBAM rules, would target embodied emissions rather than geography, simultaneously incentivizing greener production and leveraging allied support.

Instead, importers now pay a repetitive toll for the privilege of uncertainty. Bank of America’s tariff pass‑through dashboard shows that the Consumer Price Index for tariffed goods is running 2.2 percentage points above the headline CPI; core inflation, which the Federal Reserve cites for policymaking, embeds roughly 0.7 percentage points of tariff drag. The Fed, therefore, faces a cruel trade‑off: tolerate higher inflation or hike interest rates into a decelerating real economy—both pathways further erode living standards.

Lessons in Economic Statecraft:

The key takeaway from this analysis is the importance of learning from past mistakes and applying strategic foresight in economic decision-making.

A century of trade policy scholarship offers three recurrent lessons, all applicable here. First, supply chains seek the path of least resistance; barriers reshape rather than remove them. Second, distributive effects matter: Policies that compress consumer welfare without visible industrial gains lose political legitimacy quickly. Third, credibility trumps scale: If partners believe duty hikes are fleeting, they delay concessions; if they gauge them as permanent, they build alternatives, eroding the initiator’s influence.

The United States, by imposing tariffs without a detailed industrial conversion plan or a negotiation timetable, faces a dual setback: allies question Washington’s commitment while adversaries seek diversification. Meanwhile, every month that passes, new routes are baked into corporate enterprise resource planning software, raising the switching cost of reversing the policy.

Calculating the Cost of Political Theatre

Washington’s tariff barrage was conceived as a high‑stakes gambit to coerce supply‑chain realignment and renegotiate trade terms on favorable ground. The empirical footprint now tells a different story. The United States shoulders the steepest welfare loss at ‑2 %, translating into over half a trillion dollars annually. Households face annual bills up to $ 5,000, with the poorest paying the highest income share. Indirect Chinese content evades most duties by rerouting through Mexico and Southeast Asia, blunting strategic decoupling while creating a compliance labyrinth.

Global trade volume shrinks, yet many allies capture diverted demand, and some accelerate steps to dilute dollar dominance. Capital spending in frontier technologies decelerates under tariff‑induced uncertainty. In sum, the policy functions less as leverage and more as economic self‑harm, simultaneously shrinking the pie and the US slice.

A richer, data‑driven perspective thus converges on a blunt verdict: tariffs deployed as spectacle bleed credibility, competitiveness, and, most unambiguously, cash. Arithmetic has broken through the noise, reporting a policy that taxes the present to purchase an illusion of control over a rapidly reorganizing global economy.

The original article was authored by Francesco Paolo Conteduca, an Economist at the Bank of Italy, along with two co-authors. The English version of the article, titled "Roaring tariffs: The global impact of the 2025 US trade war,” was published by CEPR on VoxEU.