Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

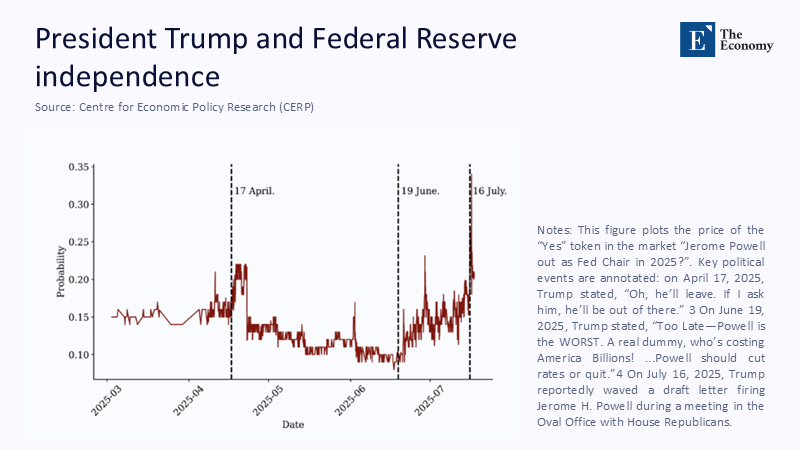

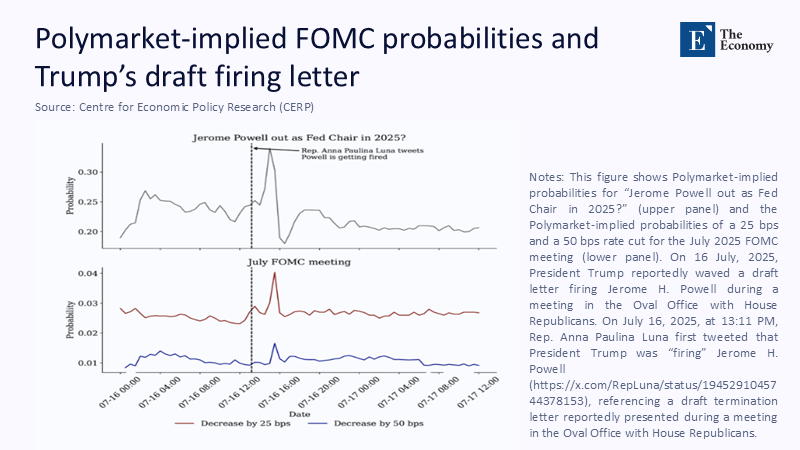

In the 24 hours before scheduled Federal Open Market Committee meetings, US equities have historically delivered an average excess return of roughly 49 basis points—a phenomenon economists call the “pre-FOMC announcement drift.” It’s a striking statistic because it captures markets doing precisely what we’re told they do best: anticipate. Yet notice what it also reveals. Those price moves don’t tell us how the FOMC will vote; they indicate that investors are reacting to the approach of a decision concentrated in the hands of just 12 voting officials. This is just one example of how markets can misread decisions made by a few. Markets can and do aggregate public expectations, but they remain one step removed from decisions made by small, insulated groups who hold the decisive information—and who typically don’t trade on it. That gap matters far beyond monetary policy. If we treat prediction markets as oracles for outcomes controlled by a handful of principals, we will mistake attention for insight and confuse liquidity with knowledge. The price is not the vote.

Reframing the Core Claim: From “Prices Know Best” to “Markets Without Principals”

The standard story says that when information arrives, markets immediately and efficiently price it—an ethos reinforced by the efficient-markets tradition, in diffuse, competitive settings, that’s often a valid approximation. But outcomes driven by a small, legally empowered committee—an FOMC, a cabinet, a university board of trustees—fit a different regime. There, the outcome is a discrete act by a tiny set of principals who may hold private information, operate under confidentiality, and are normatively constrained from trading on their knowledge. The market’s price is therefore a second-order object: it aggregates beliefs about what a few people might decide, not the decision itself. We should call these cases markets without principals. The FOMC’s formal structure—seven governors, the New York Fed president, and four rotating bank presidents—underscores the point: a dozen votes, eight meetings a year, and thick norms against leaks and self-dealing. Treating a public betting line as if it were those votes is a category error.

What the New Numbers Say

Over the last two years, crypto-native prediction venues drew unprecedented attention, with Polymarket’s monthly volume in November 2024 reportedly surging by more than 37,000% year-over-year. At the same time, empirical debates about accuracy intensified: one recent preprint finds Polymarket outperformed polls in key swing states in the 2024 US election, while critics countered that markets “did not nail” the cycle. The lesson isn’t that markets are useless—it’s that they are context-dependent instruments whose performance varies with who holds the levers of decision and who is allowed to trade. In parallel, canonical finance results remind us why perfect efficiency is unattainable when some information remains private and costly to acquire. Where predictions hinge on small-group discretion, the informational friction is especially acute. Even manipulation research is mixed: many lab and field studies suggest limited, transient effects, but fresh field experiments in 2025 show shocks can persist for weeks in thin markets. In short, the data justify qualified confidence, not blind faith.

Insider Signals Without Insider Trading

Some argue that insider trading itself improves price discovery. There’s evidence—much of it in corporate settings—that certain forms of (legal or quasi-legal) insider activity correlate with more informative prices or faster price discovery. But that logic doesn’t port cleanly to public-policy decisions. We do not—and should not—invite cabinet officials, central bankers, or school superintendents to trade on material nonpublic information. The challenge is to approximate the informational benefits of insider signals without permitting insider trading. That is feasible. Consider the evidence that superforecasters—trained aggregators of public information—have repeatedly outperformed not only lay crowds but also, at times, analysts with classified access. Combine that with decision-proximate disclosures: structured, time-stamped guidance on agendas, timing, and possible decision sets, released by institutions ahead of meetings. The combination narrows uncertainty legally and ethically, letting public forecasts key off credible signals from the principals’ process rather than off rumor or liquidity shocks.

A Blueprint for “Decision-Proximate Forecasting” in Education and Finance

Educational systems face many decisions with concentrated authority: closing or reopening schools, adopting a statewide curriculum, and appointing a president or superintendent. Treating open betting prices as if they were board votes courts error. Instead, we should build decision-proximate forecasting (DPF) programs: internal or sanctioned external tournaments with clear scoring rules, diverse forecasters, and transparent question design, paired with institutional pre-commitments about decision calendars and option sets. The method draws on forecasting platforms used in public-policy contexts and on the documented strengths of superforecasters. Technically, DPF relies on three pillars. First, signal calendars—weekly disclosures that confirm when and how decisions will be made. Second, option disclosure—enumerated decision menus (e.g., “Option A: close three campuses; Option B: close five”). Third, scored forecasting—Metaculus-style or Good Judgment-style tournaments that reward calibration and update discipline. The effect is to translate opaque, insider-controlled decisions into a series of publicly auditable signals without opening the door to prohibited trading. The potential of DPF to revolutionize forecasting in education and finance is a reason for inspiration and hope.

Anticipating the Hard Questions

Aren’t markets still better than pundits? Often, yes; the election-year evidence for markets’ relative accuracy is objective, though contested, and it’s strongest when no single actor can deterministically flip the outcome.

What about manipulation? Classic work finds manipulation tends to wash out, but very recent field experiments show durable effects where liquidity is thin and incentives are skewed—conditions common in niche policy markets.

Isn’t information leakage already visible in prices? Sometimes. The pre-FOMC drift is consistent with systematic expectation-setting, but the drift doesn’t tell us how those 12 votes will land.

Should we bless insider trading to boost efficiency? Not in public institutions. The legal, ethical, and trust costs would swamp any gains. DPF is a lawful substitute: it raises the signal-to-noise ratio by codifying institutional disclosures and then letting scored forecasters—not anonymous whales—interpret them in real time.

The Regulatory Angle: Clearer Guardrails, Richer Signals

US regulators have swung between tolerance and skepticism toward event contracts. In 2022, the CFTC penalized a major crypto prediction venue and forced non-compliant wind-downs; in 2024, a federal court held that the agency overstepped in blocking a rival’s political contracts, with appellate review ongoing; in 2025, legacy platforms sought accommodations to continue operating. This moving target illustrates why relying on retail prediction markets as standalone policy instruments is risky for public institutions. A more sustainable path is two-track: (1) keep markets where they are most defensible—diffuse, measurable outcomes with many independent contributors—and (2) institutionalize DPF where outcomes turn on small-group discretion. Regulators can help by encouraging standardized pre-decision disclosures from public bodies, much as securities rules standardized corporate disclosure, which research suggests can improve price informativeness by lowering acquisition costs and broadening access. The aim is not to shut markets down, but to route them toward the problems they’re best suited to solve.

Method Notes: How We Estimated What We Couldn’t Directly Observe

Where hard counts exist—FOMC composition and meeting cadence; specific enforcement orders and court rulings; documented platform volumes and year-over-year changes—those figures anchor the analysis. When precise, comparable statistics are unavailable (e.g., the share of discretionary, small-group public decisions across sectors), transparent proxies stand in: formal voting membership and meeting frequency of monetary policy committees; the presence or absence of public decision calendars; and the existence of pre-commitment norms for principals. Market-accuracy evidence from 2024–2025 is synthesized by weighting sample coverage (national versus swing states), timing, and whether ex ante probabilities were scored with proper rules. Manipulation risk is assessed by juxtaposing earlier experimental and field results with a 2025 randomized-shock study indicating persistence in thin markets. The throughline is not a triumphalist verdict for or against markets but a design claim: align forecasts with the actual decision-makers and pair them with lawful, decision-proximate signals.

Practical Implications for Educators, Administrators, and Policymakers

For school systems and higher-education institutions, the cost of misreading a small committee’s decision can be high—misallocated budgets, eroded trust, and policy whiplash. Replace the habit of pointing to a betting line (or to any single metric) with DPF embedded in governance. Universities and districts should publish rolling decision maps—dates, options, and evidentiary inputs—and commit to a minimum pre-decision disclosure window. They should run small forecasting tournaments that include staff, faculty, students, and external subject-matter experts, scored for calibration and updated regularly. Central banks and finance ministries can adopt the same template: richer pre-meeting signaling about decision menus, paired with expert forecasting tracks that surface minority-view risks without pressuring the principals to leak. The pay-off is not clairvoyance; it is preparation—budgets, staffing, and curricula that anticipate plausible branches rather than anchoring to the last headline price. This is how we respect both independence and transparency.

Answering the “But the Crowd Beat the Polls” Refrain

Markets indeed shone in some high-salience races in 2024, and it’s equally valid that single-actor “whales” raised questions about how much of that predictive edge reflected information versus capital and conviction. The most credible synthesis is straightforward: when millions of dispersed actors collectively influence outcomes—voters, moviegoers, shoppers—liquid markets often summarize diffuse information better than surveys. When a handful of principals control the outcome directly and credibly guard their information, prices can be directionally right yet decisively wrong. That is not an indictment of markets; it is a reminder of scope conditions. Robust governance demands building institutions—not just exchanges—that convert insider-adjacent process information (timelines, options, constraints) into public signals the rest of us can reason about, test, and learn from. That is the promise of decision-proximate forecasting. It brings the principals’ process into view without compromising integrity.

From Odds to Options

We opened with the pre-FOMC drift: a number that showcases market anticipation and exposes its limit. Prices spike before a vote because the world is waiting on a dozen people. That is precisely the class of problem where public markets, no matter how sophisticated, struggle to recover the decisive information. As prediction venues boom and headlines treat odds as verdicts, we need a more honest architecture for policy-relevant foresight—one that complements markets rather than worships them. Decision-proximate forecasting does that work. It combines lawful, structured disclosures from the principals with scored, accountable forecasting by trained generalists. For education, finance, and beyond, the call to action is simple: stop pretending that betting lines are ballots. Publish decision maps. Run tournaments that reward calibration. Measure what the principals will decide, not what a feed says in the fever of the moment. That is how we protect independence, improve preparation, and raise the signal-to-noise ratio where it counts.

The original article was authored by Barry Eichengreen, a George C. Pardee and Helen N. Pardee Professor of Economics and Political Science at the University of California, Berkeley, along with two co-authors. The English version of the article, titled "Under pressure? Central bank independence meets blockchain prediction markets," was published by CEPR on VoxEU.

References

Aktas, N., de Bodt, E., & Van Oppens, H. (2008). Legal insider trading and market efficiency. Journal of Banking & Finance, 32(7), 1379–1392.

Better Markets. (2024, Nov. 13). Prediction markets did NOT nail the 2024 election.

Bloomberg. (2025, Jan. 14). Predictions platform Polymarket’s 2025 gets off to a rocky start (newsletter report on 37,700% YoY monthly volume surge).

Brownstein Hyatt Farber Schreck. (2025). Kalshi v. CFTC challenges contracts on political events (case summary).

CFTC. (2022, Jan. 3). CFTC orders event-based binary options markets operator to pay a $1.4 million penalty (Press Release 8478-22).

Cleary Gottlieb. (2024). Elections betting pays off—for now: Implications for future event contracts.

Dentons. (2024, Oct. 1). Kalshi v. CFTC: Effect on the CFTC’s rulemaking and a new era for event contracts.

Federal Reserve Board. (2025). The Fed Explained—Who We Are (FOMC membership and structure).

Good Judgment. (2024). Full marks from The Economist (performance notes).

Good Judgment. (2024). Superforecasters vs. FT readers: Results of an informal contest in 2023.

Good Judgment. (2024). 2024 in review (highlights and statistics).

Grossman, S. J., & Stiglitz, J. E. (1980). On the impossibility of informationally efficient markets. American Economic Review, 70(3), 393–408.

Hanson, R., & Oprea, R. (2009). A manipulator can aid prediction market accuracy. Economica, 76(302), 304–314.

Iowa Electronic Markets / University of Iowa papers compilation. Market design, manipulation, and accuracy in political prediction markets (survey extracts).

Lucca, D. O., & Moench, E. (2015). The pre-FOMC announcement drift. Journal of Finance, 70(1), 329–371 (NY Fed Staff Report 512, revised 2013).

Metaculus (arXiv preprint). (2023). Evidence from a real-world forecasting tournament.

Polymarket coverage (Bloomberg, July 2025). Polymarket set for U.S. return after deal to buy tiny exchange.

Reuters. (2025). Federal Reserve Monitor (FOMC overview; meeting frequency).

St. Louis Fed & Kansas City Fed. (2022–2025). FOMC voting rotation explained; Looking back at FOMC voting structure.

Tetlock interview. (2024, Apr. 5). Philip Tetlock on teaming up with AI. Financial Times.

The Block / Forbes / WSJ election-odds coverage (late 2024). Reports on large Polymarket positions and market-manipulation disputes.

Veiga, H., & Vorsatz, M. (2013). Affecting policy by manipulating prediction markets. (Working paper series; later journal versions show robustness/limits).

Zhang, X., et al. (2025). How manipulable are prediction markets? (arXiv preprint: randomized field shocks across 817 markets).

Comment