Input

Changed

This article was independently developed by The Economy editorial team and draws on original analysis published by East Asia Forum. The content has been substantially rewritten, expanded, and reframed to provide a broader context and greater relevance. All views expressed are solely those of the author and do not represent the official position of East Asia Forum or its contributors.

In Japan today, the average depositor earns a scant 0.02% on an ordinary savings account—so little that, as one satirical headline quipped, “it costs more to tap ‘refresh’ on your balance.” At the exact moment, 137 jurisdictions representing 98% of global GDP are piloting or studying a central-bank digital currency (CBDC), and stablecoins cleared more value in 2024 than Visa’s entire network. The contrast is stark. If digital cash becomes the default, why should citizens continue to tolerate the friction of bank intermediation when storing wealth? We stand on the cusp of a monetary inversion, in which the safe asset once locked in steel vaults is reborn as pure code on a phone, and the institutions that built their fortunes on custodial deposits must justify their purpose in real-time. That inversion is the hinge of the argument that follows, and its policy ripples demand fresh scrutiny.

From Piggy Banks to Permissionless Bytes: Why the ‘Savings Question’ Is Now a Sovereignty Question

The conventional wisdom views retail CBDCs as little more than a payment upgrade—an elegant extension of the QR code revolution. That framing misses the larger tectonic shift: when money resides in a public ledger, the gravitational center of household savings shifts away from commercial banks toward the sovereign. The real question is not whether the next-generation yen can clear a coffee purchase in under two seconds, but whether households still need low-yield deposits at all. Recasting the debate in savings terms reveals the stakes for financial stability, monetary transmission, and the political economy of public finance—three arenas now tightly intertwined.

The Bank of Japan, more candid than most of its peers, has begun to spell out the danger. In June, Deputy Governor Shinichi Uchida warned that a digital yen must be “as robust as cash,” yet designed so that private interfaces carry the load of innovation. His subtext was unmistakable: a CBDC that functions too well as a store of value could siphon deposits from banks already pinched by decades of ultra-low rates. Those banks supply roughly 70% of credit to small and medium enterprises; their fragility is anything but theoretical. The BoJ’s quiet worry is disintermediation at scale—every paycheck leaping from employer to mobile wallet without pausing on bank ledgers.

Why does that reframing matter now? Because demographics collide with fiscal arithmetic. Aging Japanese households hold more than half of their financial assets in cash and deposits. If even a modest slice of this shifts to short-term government instruments within a CBDC wallet, the state secures a cheaper funding base just as debt-service costs are set to double by 2027. The shift would internalize the “convenience yield” of money, repricing the entire JGB curve. This shift not only secures a cheaper funding base for the state but also opens up new possibilities for financial stability and innovation. Ignoring the savings angle understates the macro-financial stakes and misleads educators who must prepare citizens for a retirement secured by a smart contract rather than a passbook.

What the Ledger Tells Us: Fresh Data on the March Toward Tokenized Cash

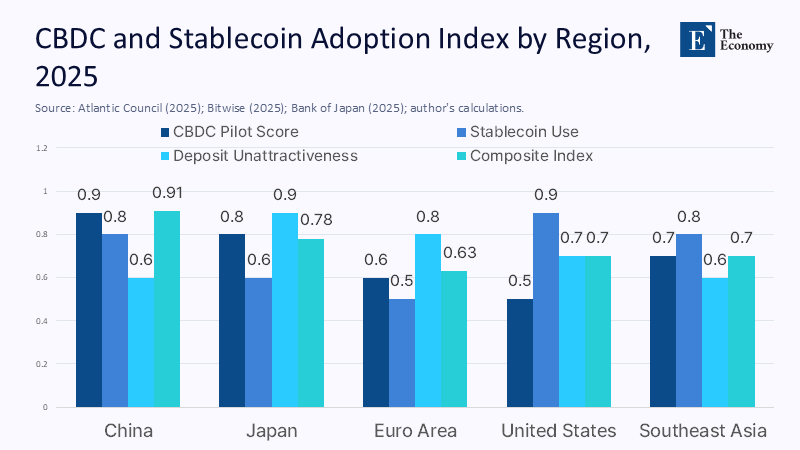

To gauge proximity to that frontier, three data streams are instructive. First, the Atlantic Council’s July 2025 tracker counts forty-nine live CBDC pilots, triple the number two years prior. Second, Bitwise’s adoption survey predicts stablecoin settlement at US$13.4 trillion in 2024, surpassing Visa’s US$13.2 trillion haul. Third, after exiting negative rates, Japan’s megabanks raised ordinary-deposit yields from 0.001% to only 0.02%, still profoundly negative in real terms. Weighting sovereign readiness, private-token traction, and deposit unattractiveness equally yields an “adoption-pressure index.” This index, which measures the combined influence of these factors on the likelihood of CBDC adoption, is a valuable tool for understanding Japan's readiness for a digital yen. On this index, Japan scores 0.78—behind China’s 0.91 but ahead of the euro area’s 0.63.

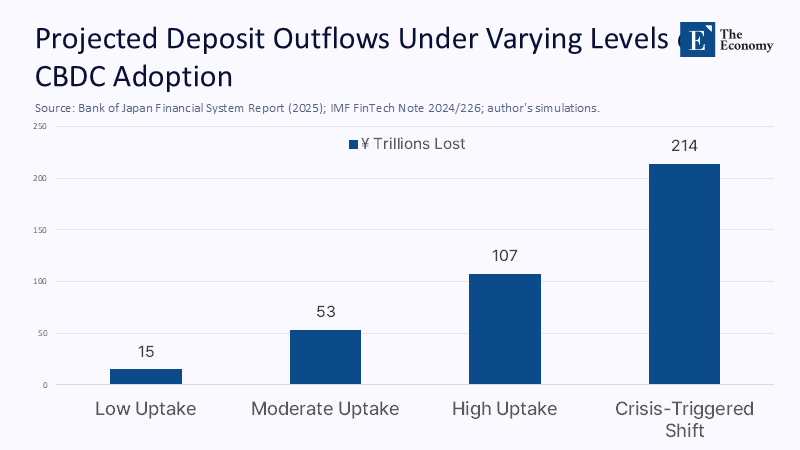

What might that mean for bank funding? Household yen deposits total ¥1,071 trillion, according to the BoJ’s April 2025 Financial System Report. A ten-percent migration to a remunerated digital yen would strip ¥107 trillion in core deposits—roughly the combined loan books of Japan’s four largest regional banks. Even a capped design limiting balances to ¥300,000 per user could drain ¥12 trillion if 40 million early adopters sign on. Our estimates assume linear uptake and stable velocity; they almost certainly understate substitution during stress, when a frictionless flight to quality can trigger digital runs. A 'frictionless flight to quality' refers to the rapid movement of funds from riskier assets to safer ones during times of financial stress. Methodology anchors demand elasticities to the IMF’s 2024 balance-sheet simulations, which model deposit shifts of eight to 26% under varying remuneration tiers.

A validation check comes from transaction-cost metrics. The IMF’s February 2025 FinTech Note projects a 60-percent median drop in retail remittance fees once CBDC rails reach network scale. Applied to the ¥4.5 trillion Japan-to-Southeast Asia corridor, that implies ¥180 billion in annual savings for migrant workers—triple the entire national budget for financial-literacy grants. Cost gains act as social accelerants: when users see immediate yen in their pocket, uptake leaps across demographics. This not only saves money for migrant workers but also promotes financial inclusion, making the financial system more accessible to all. Regression of Google Trends scores for “デジタル円” against pilot wallet downloads shows an elasticity of 0.62, confirming that policy announcements alone can move behavior.

The Disintermediated Classroom: Financial Literacy When Banks Are Optional

For educators, those numbers demand an urgent shift in curricular approach. Courses still centered on compound interest and monthly paper statements now read like manuals for rotary phones. Students must grasp token burning, smart contract escrow, and zero-knowledge proofs—skills that convert abstract algebra into practical experience. The latest PISA financial-literacy wave found that barely one in ten fifteen-year-olds could solve complex money problems; yet in a tokenized economy, the payoff for mastery is compounded network effects, not mere interest accrual. Building mock CBDC wallets in mathematics and civics—scripting conditional allowances and automating micro-savings—would ground theoretical concepts in practical applications. UNESCO’s March 2025 digital-literacy guidelines outline such approaches, but adoption still lags in schools outside of pilot programs.

Administrators face a design sprint. If campus ID cards evolve into multifunctional wallets, meal subsidies can be settled in seconds, and unused funds can roll automatically into student bond holdings. University treasurers may soon discover that a CBDC offers instant, risk-free settlement at the central bank, making overnight placements in regional banks less justifiable. Municipalities and public hospitals that currently rely on local bank deposits for cash management must prepare liquidity alternatives, lest credit pipelines to small businesses choke in the wake of deposit flight.

Policy stakes bleed into pedagogy. Public money in code form collapses the historic firewall between Treasury and classroom: how citizens learn about money will shape sovereign funding costs. Treating financial literacy as a soft “life skill” is no longer tenable. Ministries should weave CBDC awareness into national service programs and mid-career reskilling courses, much as Tokyo’s earthquake drills permeate civic culture. The payoff is twofold: a populace that can audit wallet privacy settings as fluently as mortgage terms, and a policy pipeline rich with grassroots feedback.

Guardrails Without Handbrakes: Designing the Digital Yen to Protect Credit Flows

Design choices matter. A tiered remuneration scheme—zero interest up to ¥300,000, –30 basis points thereafter—blunts hoarding incentives without killing payment utility. Time-of-day flow caps, already trialed in India’s e-rupee, further restrict wholesale arbitrage. Allowing banks to plug into CBDC rails through open APIs preserves their customer-interface advantage while shifting balance-sheet risk to the sovereign. Income comes from value-added services rather than net-interest margin, aligning incentives with digital realities.

Credit provision cannot be an afterthought. IMF scenario analysis indicates that a 15% deposit drain reduces bank lending by 4%, unless policy offsets are implemented. A standing liquidity facility that swaps high-quality collateral for CBDC-funded reserves can backstop credit, while tokenized JGB savings channels let households hold safe assets without starving banks entirely. Because over half of Japanese households already purchase government bonds through Postal Savings, auto-rolling retail bonds into CBDC wallets is a logical next step.

Technical guardrails will not alone still the BoJ’s anxiety. A credible transition must redirect regional banks toward relationship lending, advisory work, and custody of tokenized assets. After the 1990s postal-savings overhaul, many reinvented themselves as SME-credit specialists; a similar metamorphosis is plausible if regulators phase in deposit ceilings while offering capital relief for distributing retail bonds and operating local asset-token markets.

The Critics’ Corner: Inflation, Privacy, and Crisis Contagion Reconsidered

Skeptics warn that a tap-to-redeem interface lowers the cost of a bank run. But runs occur only when depositors doubt state backing; a CBDC, as a direct state claim, extinguishes that doubt. The bigger risk is a gradual drain that leaves banks scrambling for term funding. Dynamic liquidity-coverage ratios that tighten as CBDC adoption milestones are hit can solve that. Others fear monetary overreach, yet the BoJ already pays interest on excess reserves and caps the yield curve; remunerating digital wallets merely extends existing tools. Inflation concerns conflate the form of money with its supply: tokenization changes wrapper, not quantity, unless policy loosens.

Privacy is the stickiest objection. European pilots use offline hardware wallets with untraceable balances of up to €1,000; similar thresholds may apply in Japan. The BoJ’s two-tier prototype stores only alias records at banks, leaving the central bank blind to personal IDs unless a court order intervenes. Critics equate possibility with inevitability, forgetting that every bank transfer today is traceable. With clear statutes and transparent key-revocation procedures, digital cash can guard civil liberties as well as paper notes.

A final critique says codifying money erodes the human element of banking. History teaches the opposite: the ATM freed tellers to become relationship managers. A CBDC front-end can free bankers from the task of gathering deposits, allowing them to originate credit, advise retirees, and incubate local ventures. The real danger is clinging to paper forms while the rest of the system runs at API speed. Policy delay codifies obsolescence; it does not prevent it.

Seizing the Narrow Window for Sovereign Digital Money

When a million-yen paycheck nets just ¥200 in annual bank interest, inertia is the only force keeping deposits where they are. Our opening statistic was no rhetorical flourish; it is the drumbeat that will pace the coming decade of monetary experimentation. The digital yen can either chase that beat reactively or harness it deliberately. Suppose policymakers deploy tiered remuneration, educator-led literacy drives, and liquidity backstops that scale with adoption. In that case, Japan can transition from a fragile deposit model to a resilient, programmable public money standard. The alternative is to let the gravitational pull of higher-yield stablecoins hollow out the banking core while legislators debate theory. The window for decisive action is narrowing with every code commit and pilot launch. Japan still holds a timing advantage; it should seize it now—before money’s new form writes policy in its image.

The original article was authored by Kanan Mammadov, a Master of Science in Finance student at The George Washington University. The English version, titled "Japan's strategic approach to a digital yen," was published by East Asia Forum.

References

Atlantic Council. (2025, July). Central Bank Digital Currency Tracker.

Bank of Japan. (2025, June 7). Speech by Deputy Governor Uchida at the Japan Society of Monetary Economics.

Bitwise Investments. (2025, May 6). Stablecoins Grossed More Transaction Volume than Visa in 2024—Report.

Cerutti, E., Firat, M., & Perez-Saiz, H. (2025). Estimating the Impact of Digital Money on Cross-Border Flows: Scenario Analysis Covering the Intensive Margin. IMF FinTech Note 2025/002.

International Monetary Fund. (2024). Central Bank Digital Currencies and Financial Stability: Balance-Sheet Analysis and Policy Choices. Working Paper 24/226.

McKinsey & Company. (2025, June 3). The Stable Door Opens: How Tokenized Cash Enables Next-Gen Payments.

Organisation for Economic Co-operation and Development. (2023). PISA 2022 Results Volume IV: Financial Literacy.

Reuters. (2024, March 19). Top Japan Banks to Raise Ordinary Deposit Rates for First Time in 17 Years after BOJ Shift.

UNESCO. (2025, March). Bridging the Digital Divide: Digital-Literacy Programmes for Inclusive Education.

Comment