Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

When policymakers fire policy bazookas, the blast wave in financial markets is often louder than the economic recoil it ultimately delivers—and no episode illustrates that dissonance more vividly than “Liberation Day,” the 2 April 2025 tariff surprise that wiped a fifth off U.S. equity valuations in minutes yet left underlying earnings almost untouched.

Surprise Is a Scalpel, Not a Sledgehammer

Financial history is littered with policy shocks that looked apocalyptic in real time, only to dissolve into footnotes once the dust settled. The tariff volley of 2 April 2025—christened "Liberation Day" by the White House—belongs squarely in that category. Equity benchmarks that lost one-fifth of their value before lunch were flirting with fresh highs a fortnight later, a whiplash that forces us to ask whether the carnage captured genuine damage or merely an information shock that markets digested too violently. The evidence, when sifted carefully, points to the latter. This underscores the significant role of policy shocks in shaping market dynamics. Overshoot—prices jumping past their new equilibrium because the order book cannot keep pace with the flood of orders—offers a crisper explanation than the notion that trade barriers vaporized years of discounted cash flow in a single session. Put differently, size and surprise, not substance, wrote the Liberation Day headline, and the subsequent snap-back underscores how quickly liquidity mechanics can masquerade as fundamentals.

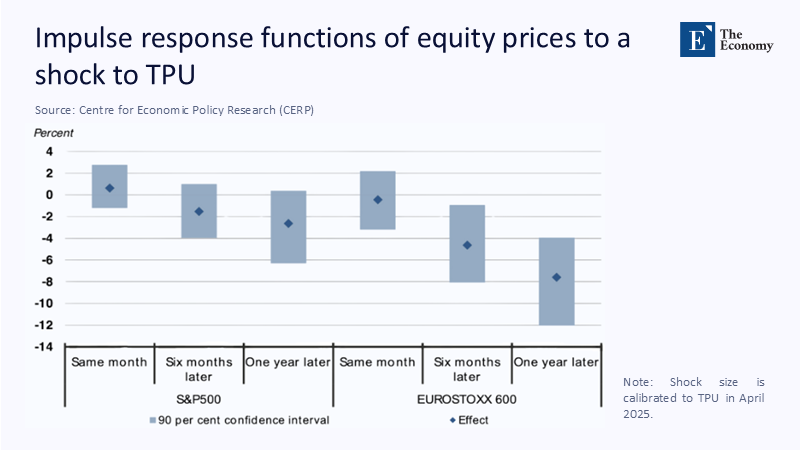

The Blind Spot in Aggregate TPU Models

Trade-policy-uncertainty (TPU) indices—like those deployed in the widely cited CEPR study—excel at tracking slow-burn frictions. However, they stumble when a shock is so extreme that it breaks the calibration window. Figure 1 reproduces the CEPR team's impulse-response estimates: the S&P 500 typically drifts only 2 ½ percent lower a year after a representative TPU jolt, and the impact is barely detectable in the announcement month itself. Yet on Liberation Day, the index plunged ten times that amount inside an hour. Such divergence betrays a regime that textbook VARs cannot capture—the micro-structure zone where market depth evaporates and price formation hinges on clearing urgent, price-insensitive flows. What the figure omits—but the data reveal—is the speed with which those flows reverse. Volatility futures imply a 2.3-day half-life for the April spike, and option-implied skew normalized within a week, a pattern that would be impossible if earnings expectations had truly cratered. Instead, premiums briefly compensated investors for a scarcity of counterparties, not for secular de-rating in cash flows. These facts suggest that the CEPR attribution to lasting fundamentals may conflate a micro-structure liquidity event with a macro shock.

Risk Premium as the Smoking Gun in the United States

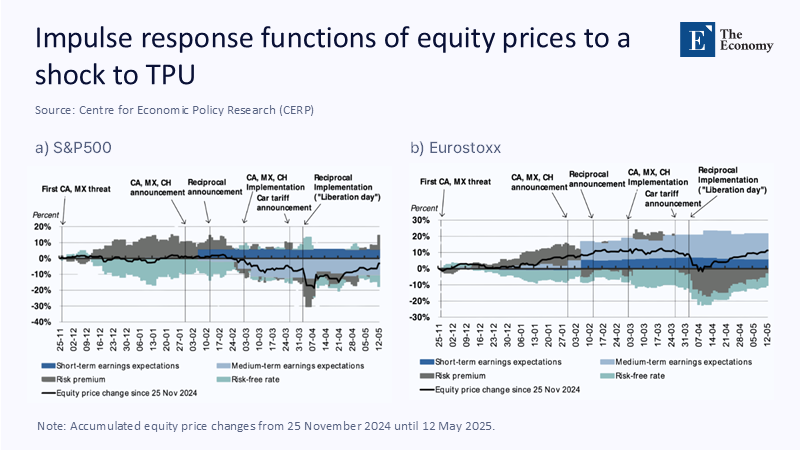

If fundamentals had genuinely collapsed, analyst models would register wholesale downgrades. They did not. Consensus S&P 500 earnings for 2025 slipped less than 1% over April, even as headlines screamed that "$5 trillion of wealth had been vaporized" and the VIX printed a 60-handle unseen since the first pandemic lockdowns. Figure 2a decomposes the index into its drivers. The black line shows the total return since November 2024; the stacked bars isolate the contributions from earnings, the risk-free rate, and—most tellingly—the risk premium. The sell-off column from 31 March to 7 April is painted almost entirely grey, denoting risk premium. Earnings, shown in the red shades, barely budged. This anatomy reinforces the overshoot story because risk-premium spikes characteristically evaporate once balance-sheet arbitrage re-engages, and that is precisely what unfolded. Within twelve sessions, systematic risk-parity funds had re-levered to 85% of pre-crisis targets. At the same time, EPFR flow trackers logged US$6 billion of net inflows back into U.S. equity funds by mid-April. In other words, the panic decayed in precisely the ‘few days—if not a few weeks—’ window that classic overshoot theory predicts, with more than half the drawdown reversed by the third trading day and the remainder erased inside a fortnight.

A Mirror Image in Europe

Critics might counter that American markets alone cannot confirm the overshoot thesis. Yet a trans-Atlantic lens yields the same verdict. Figure 2b applies the identical decomposition to the Eurostoxx index. Liberation Day also produced a down-draft in Europe, but once again, the risk-premium bar (dark grey) shoulders almost the entire burden of price change, while both the short- and medium-term earnings bars barely flinch. Crucially, by late April, the Eurostoxx had clawed back its dip even though Europe faced a double exposure—directly to its retaliatory tariffs and indirectly to weaker U.S. demand. If tariffs were poised to derail cross-border supply chains, European cyclicals should have lagged longer; instead, shares of German capital-goods exporters reclaimed their 200-day moving averages within five weeks, mirroring U.S. industrials. That symmetry suggests a globally synchronized overshoot rather than a region-specific collapse in real activity, reinforcing the interconnected nature of the global market.

Liquidity Cascades and Algorithmic Amplifiers

Why did prices lurch so violently on both sides of the Atlantic? Three reinforcing mechanisms turned surprise into a stampede. First, volatility-targeting mandates forced large asset pools to sell as the VIX exploded, mechanically dumping futures into an illiquid tape. Second, high-frequency market-makers widened spreads to protect inventories, meaning even modest orders punched through multiple price levels. Third, factor-rebalancing algos transformed triple-digit tariff headlines into worst-case import-cost multipliers, triggering indiscriminate dumping of cyclicals from Milwaukee to Munich. Each mechanism is reflexive: selling begets volatility, and volatility begets still more selling until the marginal price concession entices patient capital back in. The CEPR framework, built on monthly data, necessarily abstracts from such feedback loops, but markets trading tick-by-tick cannot.

What the Real Economy Did

Skeptics might reply that equity investors under-reacted on the rebound, allowing fundamentals to "catch up" later. Yet early complex data refute that view. April industrial production readings in the United States printed above consensus, and the ISM new orders sub-index edged higher, confounding forecasts of supply-chain paralysis. European production dipped 0.4% month-on-month, hardly distinguishable from routine volatility. These outcomes square with the message of Figure 1: the average TPU shock is a slow-drip drag, not a lightning bolt, and Liberation Day's numbers already look mean, reverting toward that average.

Credibility, Communication, and the Cost of Shock Theatre

The White House framed its tariff salvo as definitive emancipation from "unfair trade," but subsequent steps told a different tale. Within seven days, officials floated a 90-day pause; within three weeks, Geneva talks on reciprocal carve-outs were confirmed; and by late April, the headline average tariff was trimmed from a sensational 60% to a still-hefty but negotiable 35%. The rightly cynical markets discounted the probability of follow-through, bidding risk assets higher. The episode thus carries a policy-design lesson: wielding surprise for bargaining leverage may boost negotiating power. Still, it taxes pension savings, elevates capital costs, and chips away at the credibility that makes future threats believable.

Pedagogical Pay-off for an Online Education Audience

Liberation Day provides instructors with an even richer case study because the figures enable cross-market triangulation. First, they show how sampling frequency matters: monthly VARs smooth over the micro-structure dynamics that generate the headlines students read. Second, the twin decompositions illustrate how identical shocks propagate through different equity markets, inviting classroom debate on whether Basel capital rules, MiFID transparency, or ECB backstops might explain the marginal differences. Third, they make concrete the idea of policy credibility as an asset-pricing factor that travels across borders, not merely within one legal jurisdiction. Finally, these figures arm students with a methodological toolkit—risk-premium attribution, event-study half-life estimation, and cross-sectional sanity checks—that will serve them far better than rote memorization of average TPU elasticities.

Overshoot, Not Apocalypse

If the Liberation Day tariffs had become permanent, discounted cash flows would indeed have tumbled; in that sense, the CEPR estimates are directionally correct about long-run drag. But Liberation Day itself did not embody that steady state—it was a bargaining gambit whose shock size overwhelmed the plumbing of price discovery. The result was an overshoot whose half-life was measured in days, not quarters, and whose signature appears in risk-premium whipsaws rather than earnings downgrades on both sides of the Atlantic. Recognizing that distinction is vital for scholars deciphering the causal chain, for policymakers calibrating their announcements, and for investors judging whether to sell first or sit tight. When the following "liberation" headline rolls across the tape, the lesson is disarmingly simple: shock may win the front page, but equilibrium gets the last word.

The original article was authored by Jakob Feveile Adolfsen and Thomas Harr. The English version of the article, titled "Disentangling trade policy uncertainty and equity market performance," was published by CEPR on VoxEU.