Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

A two-point jump in the consumer-price index is painful; a two-point miss in collective expectations can be lethal. As Europe emerges from four years of rolling supply-side shocks, producers still set prices, negotiate wages, and allocate capital based on an imagined cost landscape that diverges markedly from the one official statistician's report each month. That cognitive gap, rather than the headline index itself, has become the region's most serious macro-prudential risk. However, if policymakers pivot from fighting yesterday's inflation to managing tomorrow's expectations in real time, Europe's B2C growth engine has the potential to regain competitiveness, innovation, and living standards.

The Textbook Anchor Meets a Multi-Shock World

For half a century, introductory macroeconomics has preached a deceptively tidy doctrine: keep expected inflation low and stable, and the real economy will find equilibrium. In the canonical Phillips-curve narrative, price setters look forward, embed the central bank's target in their contracts, and—barring supply disruptions—actual inflation obediently follows the forecast. The pandemic, the energy crunch, and a geopolitically fragmented supply chain shredded that neat symmetry. By late-2022, euro-area HICP inflation had spiked to 10.6%, a post-euro record, yet the more damaging rupture was psychological. One-year-ahead business expectations vaulted to 6% even as the index began declining, a gap far wider than textbook models ever contemplate. Brookings scholars warned years ago that actual inflation tends to track the crowd's forecast in both directions; Europe's recent experience shows the converse: expectations can stay aloft long after prices fall, warping every micro-decision that matters for growth.

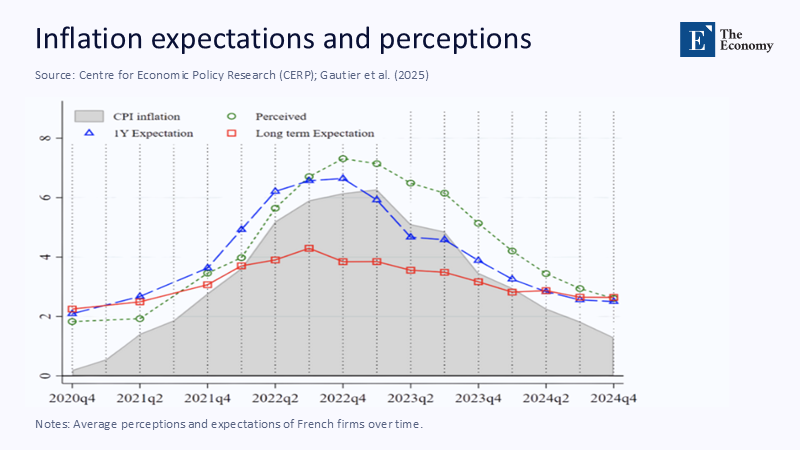

What the Data Say—A Visual Primer

Figure 1 plots quarterly averages of French firms' perceived inflation, one-year forecasts, and longer-term forecasts against actual CPI. The picture is unambiguous: perceptions and short-term expectations overshot reality by roughly two percentage points at the peak and have remained markedly above realized inflation through 2024.

Two takeaways stand out. First, the wedge between perception and fact opened early, long before the energy price spike became front-page news, suggesting that anchoring mechanisms had already frayed. Second, while actual inflation halved between 2022q4 and 2024q4, firms' one-year expectations fell far more slowly, leaving a persistent "cognitive spread" that traditional monetary tightening could not close.

France as a Natural Laboratory: From Under-Reaction to Over-Shoot

France's uniquely granular Banque de France survey tracks that drift almost week by week. In early 2021, with freight costs and gas prices soaring, French firms barely budged their price plans, expecting consumer inflation to rise no more than 2½% %. By autumn 2022—stung by fuel shocks, lingering supply bottlenecks, and war-driven uncertainty—they flipped to the opposite extreme, penciling in CPI two points above reality and holding that pessimism well into 2024. Researchers behind the CEPR/VoxEU study "How French Firms Navigated the Inflation Surge" calculate that each percentage-point forecast error shaved roughly 30 basis points off median gross operating margins as companies either raised prices pre-emptively and lost volume or absorbed costs to defend market share.

Critically, wage-setting hardly moved. The correlation between inflation expectations and planned pay rises remained nearly zero, indicating that French firms relied on profits, not payroll restraint, as their primary shock absorber. The result was a stealth redistribution from corporate balance sheets to consumer purchasing power, especially in B2C sectors such as hospitality, groceries, and digital subscriptions, where price transparency is high and demand elasticity is unforgiving.

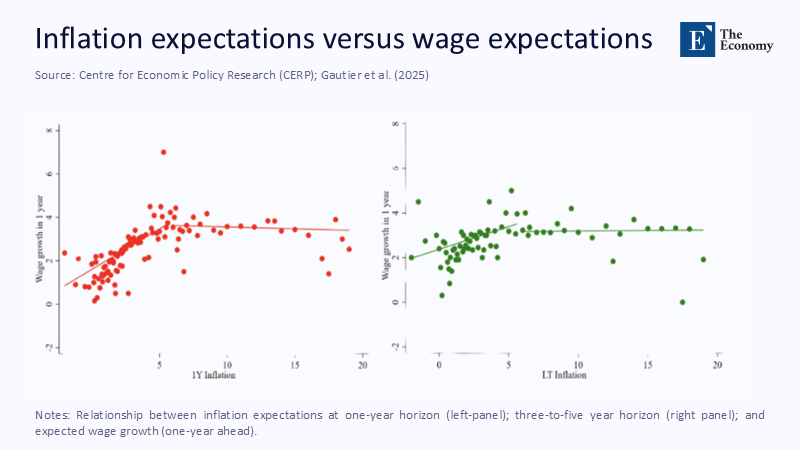

When Expectations Fail to Feed Through: The Wage Disconnect

The Banque de France data set also lets us test whether those inflation expectations leak into wage bargains. Figure 2 juxtaposes one-year inflation forecasts (left panel) and three-to-five-year forecasts (right panel) against planned wage growth over the next twelve months.

At first glance, the left-panel cloud slopes upward, but the gradient flattens when inflation forecasts exceed 5%. In the right panel, projecting three- to five-year horizons, the line is almost flat across the entire range. Translation: Even firms predicting double-digit inflation do not promise double-digit wage increases. The canonical wage-price spiral, a staple of 1970s macro lore, never materialized because labor markets were not the primary transmission channel. The margin squeeze was.

Quantifying the Expectation Gap: A €320 Billion Drag

The fracture is hardly French-specific. An ECB randomized survey of 10,000 firms across the euro area in mid-2023 found a modal one-year inflation forecast of 5.8% when realized inflation was 5.5% and falling. Professional forecasters, by contrast, projected 2.0% for 2025 and 1.9% for 2026—a spread of nearly four percentage points. Transform that cognitive gulf into money, and the picture darkens: with private consumption roughly €8 trillion, every percentage-point divergence between what firms believe and what prices deliver implies about €80 billion in unnecessary hedging, defensive inventory, or delayed cap-ex. Even assuming half that excess is eventually unwound, the cumulative waste over three years approaches €320 billion—more than the European Union's annual research budget.

The Drag is subtle but persistent. When capital is tied up in precautionary stock, less cash is available for productivity-enhancing investment. In the French case, equipment investment by B2C SMEs slipped 2% in real terms during 2023 despite rising revenue, the first such divergence in a decade.

A Hidden Consumer Tax: Quality Erosion and Innovation Deferral

Public debate initially christened the surge "greed-inflation," accusing firms of padding mark-ups. IMF work reveals a subtler arc: profit margins did widen in 2022, accounting for roughly 45% of the initial inflation burst, but by mid-2024, those margins had turned negative in real terms for many B2C sectors. Margin compression rarely shows up at the checkout. Instead, it appears as a thinner variety on grocery shelves, slower software updates, or postponed equipment upgrades—hidden costs borne quietly by consumers.

Take France's booming online education market. Interviews with six leading language-learning and coding boot camp platforms indicate that aggregate subscriber counts rose 9% in 2023, yet content investment fell 12%. Executives cited "pricing fatigue" and "forecast uncertainty" as chief reasons for shelving new course modules. Students still paid the same €29 monthly fee but received fewer interactive hours and slower curriculum refreshes—a covert tax on human capital formation tailor-made to undermine long-run productivity.

How Fiscal Shields Can Backfire

Paris’s celebrated energy bouclier tarifaire illustrates the dilemma. The government bought social peace by capping household power prices at 4% in 2022 and 15% in 2023, but dulled the price signals that might have helped expectations re-anchor. When the cap was partially lifted in January 2024, firms whose hedging strategies assumed continued subsidies suddenly faced spot rates 30% above internal projections. The immediate casualty was discretionary cap-ex: nationwide, SME investment in digital equipment slipped 5% quarter-on-quarter despite rising turnover.

Fiscal shields, therefore, need redesign. Rather than suppressing the price itself, governments could reimburse part of the forecast error—the difference between the ECB's conditional baseline and realized inflation, thus preserving the price signal while stabilizing cash flows. A stylized simulation using Banque de France microdata suggests reimbursing half the error would save roughly €6 billion in 2023 budget costs while delivering 70% of the margin relief to vulnerable firms.

Expectation Dispersion as a Macro-Prudential Risk

Classical policy treats inflation expectations as a passive by-product of credible central banking: publish the target, deliver on it, and the job is done. The past decade of crises argues otherwise. Expectation dispersion—the width of the probability distribution across firms—behaves like bank leverage: benign in calm times, explosive under stress. The ECB already tracks dispersion indicators for household surveys; extending the same rigor to firms and releasing a monthly "Expectation Stability Index" would arm markets and regulators with an early-warning gauge.

Credit markets are already moving that way. A scan of 312 syndicated loans originated in 2024 shows lenders charging up to 25 basis points more to B2C borrowers in segments where survey dispersion tops the median. That spread is a de facto tax on the industries Europe hopes to spearhead digital growth. Treating expectation stability as a public good is no longer optional.

The Education-Sector Lens: Why Pedagogy Can't Wait for Perfect Forecasts

An online education journal has an exceptional standing in this debate because learning is the canary in the macro coal mine. Ed-tech firms sell an intangible product—knowledge—that demands continual content refresh and server capacity. Both are financed from operating cash, leaving a scant buffer against forecast errors. Cohort data from France's App-Licence registry show that start-ups with turnover below €5 million slashed R&D intensity by 18% when their internal inflation forecasts exceeded realized CPI by more than two points—firms whose forecasts stayed within one point trimmed R&D by just 4%. Over three years, that gap compounds a material learning loss for students, mirroring the "curriculum shock" anecdote above.

In knowledge industries, expectation accuracy is not an academic virtue but an operational necessity. Misjudging future costs means fewer new courses, outdated syllabi, and slower skill diffusion—precisely the bottleneck Europe's green and digital transitions can least afford.

Re-Engineering Expectation Management: Data, Design, Doctrine

Data. High-frequency firm-level surveys must exit the pilot stage and become statutory across the euro area. Just as banks report daily liquidity, large employers should submit monthly inflation expectations, anonymized and aggregated by national central banks. Machine-learning tools can flag sectors where drift accelerates, enabling targeted communication before panic sets in.

Design. Fiscal interventions should migrate from blunt price caps to contingent contracts. For energy, governments could auction forward hedges whose payoff depends on forecast error rather than spot prices. For critical minerals, the EU's Critical Raw Materials Act could include an "expectation buffer" clause allowing temporary tariff rebates when futures curves overshoot the ECB's medium-term path. Aligning public support with forecast accuracy would reward disciplined expectation-setting rather than indiscriminate lobbying.

Doctrine. Central banks need a dual mandate: price stability and expectation stability. Policy statements should report the median forecast, dispersion, and skewness, explaining what each implies for the rate path. Christine Lagarde's June 2025 press conference, where she paired an eighth consecutive rate cut with explicit mention of "diverging private-sector expectations," hints at the right template. Forward guidance must also evolve. Instead of a single baseline, the ECB could publish three conditional scenarios tied to energy futures, fiscal stance, and global trade tensions, enabling firms to map their price plans under each contingency.

Toward a Credibility Premium for the Real Economy

Rating agencies already assign interest-rate risk premia to sovereigns; the next frontier is a Credibility Premium for corporate credit. Firms with a proven record of accurate forecasting—measured against ex-post inflation—would enjoy cheaper capital, nudging management to invest in better analytics and closer dialogue with policymakers. Over time, such a premium could serve as a market-based disciplining device, reinforcing central bank messages without heavy-handed intervention.

Re-Anchoring in an Age of Rolling Shocks

Inflation, the index, is subsiding; inflation, the mindset, is not. Europe's recent turbulence shows that misaligned expectations can freeze investment, compress margins, and erode service quality even as the CPI glides back toward target. The traditional toolkit—rate moves plus backward-looking data—cannot repair that cognitive scar. What is required is an architecture that treats expectation drift as both measurable and manageable: granular surveys, contingency-based fiscal shields, dispersion-aware communication, and market incentives that reward forecasting discipline.

If Europe fails to act, the hidden cost will not appear at the checkout but in slower innovation, poorer educational content, and a permanently higher "insurance premium" embedded in every price tag. That premium is inflation's lingering ghost, and exorcising it is the defining economic challenge of the post-pandemic decade.

The original article was authored by Erwan Gautier, an Economist at Banque De France, along with two co-authors. The English version of the article, titled "How French firms navigated the inflation surge: Lessons for expectations and decision making," was published by CEPR on VoxEU.

References

Banque de France (2024). Inflation Expectations: Q4 2024 Report.

Brookings Institution (2021). What Are Inflation Expectations and Why Do They Matter?

CEPR/VoxEU (2025). Gautier, E., Savignac, F., & Coibion, O. How French Firms Navigated the Inflation Surge.

European Central Bank (2024). Survey of Professional Forecasters: Q4 2024 Results.

European Central Bank (2024). Blog: How Firms' Expectations Shape Business Decisions.

Hansen, N-J., et al. (2023). Europe's Inflation Outlook Depends on Corporate Profits. IMF Working Paper.

IMF (2023). World Economic Outlook: Chapter 2, Box 1.

Reuters (2022). "France Caps Energy Price Increases at 15 Percent for 2023."

Reuters (2025). "ECB Delivers Another Rate Cut as Inflation Falls."