Input

Changed

This article was independently developed by The Economy editorial team and draws on original analysis published by East Asia Forum. The content has been substantially rewritten, expanded, and reframed for broader context and relevance. All views expressed are solely those of the author and do not represent the official position of East Asia Forum or its contributors.

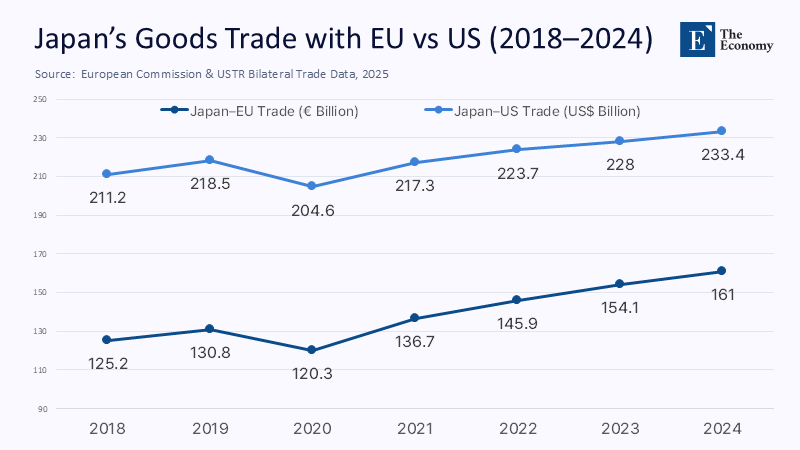

In the space of just five calendar years, the expansion in Japan-EU trade in goods and services has outpaced growth in Japan-US trade by more than two-to-one, even though the United States still looms largest in Tokyo's security perceptions. This strategic foresight is evident in the simple arithmetic that reveals a profound shift: Japan no longer equates economic security with the US alliance; instead, it is weaving a denser, multi-theater web in which Europe supplies the strategic redundancy that an ''America First " White House can no longer guarantee.

From Client State to Portfolio Balancer: A Historical Re-Reading

Following World War II, Japan adopted a two-tier strategy: subcontracting military deterrence to the United States while rebuilding its industrial capacity under the protection of a nuclear umbrella. For decades, the formula held, but three structural forces have diluted its sufficiency. First, the Emergency Economic Partnership Agreement (EPA), which entered into force in 2019, has injected momentum into trans-Eurasian commerce, pushing total EU–Japan flows up 20.4% between 2018 and 2023; the average annual growth rate has held at nearly 4% even through pandemic volatility and yen weakness. Second, the US-Japan merchandise trade has matured into a low-growth, debt-funded plateau. In 2024, exports from the United States to Japan increased modestly by 5.4%, while imports from Japan grew by less than 1%, resulting in a structural US deficit of $68.5 billion and sparking recurring tariff discussions in Washington. Third, China's coercive economic statecraft—choking gallium exports in 2023 and rare-earth shipments a decade earlier—has convinced Japanese planners that any single-source dependency is a vulnerability, whether that source is Beijing or the Beltway. Taken together, these currents impel Tokyo to behave less like a client and more like a portfolio balancer whose hedging instrument of choice is Europe. This strategic partnership between Japan and Europe is a cause for optimism in the future of trans-Eurasian commerce.

Trump 2.0 as Catalyst: Calculated Uncertainty

Donald Trump's return to the White House in January 2025 converted latent hedging incentives into explicit policy. A new tariff schedule, still in draft form but leaked to Senatorial staffers in March, threatens five-per-cent levies on automotive imports from any ally that fails to raise defense outlays toward a notional two-per-cent-of-GDP benchmark. This ultimatum falls awkwardly in Tokyo, where the Diet has already authorized a record ¥7.7 trillion (approximately US $52.7 billion) defense budget request for fiscal year 2024. Privately, Japanese officials note that the request is heavily weighted toward cyber and missile defense upgrades rather than the conventional platforms the Pentagon prefers, underscoring a philosophical divergence that tariffs cannot paper over. Trump's renewed insistence on a US energy surplus as a strategic asset sharpens the divergence: he lobbied Prime Minister Shigeru Ishiba to sign long-term offtake agreements for Alaskan liquefied natural gas (LNG) transported via an 800-mile pipeline from the North Slope—an undertaking priced at US $44 billion before cost overruns. Ishiba's interlocutors in Keidanren label the project "commercially heroic at best," pointing to shipping costs that would exceed landed prices for equivalent Qatari or Australian cargoes. Here, Trump's leverage meets its limits: the more he weaponizes tariffs and energy dictates, the more Tokyo looks for counterweights.

Counting the Rebalance: Trade, Investment and the Geometry of Dependence

The numbers illuminate the qualitative story. EU exports of goods to Japan increased from €64 billion in 2023 to €68.8 billion in 2024, a 7.1% rise that extends a five-year upward trend. Total bilateral services trade surpassed €58 billion, representing a 34.7% increase since the EEPA's first anniversary. Meanwhile, US goods exports to Japan grew to US $79.7 billion in 2024, but that reflected price effects in aerospace and LNG rather than volume expansion; on a volume basis, growth has flat-lined since 2019. Japanese foreign direct investment in Europe now stands at €212.5 billion—triple the EU's investment stock in Japan—confirming that corporate Japan is embedding its supply chains more deeply into the single market, not merely selling finished goods there. The geometrical metaphor is instructive: Europe provides Tokyo with multiple nodes of interdependence, thereby diluting the capacity of any single partner to coerce.

LNG, Green Hydrogen, and the Alaska Litmus Test

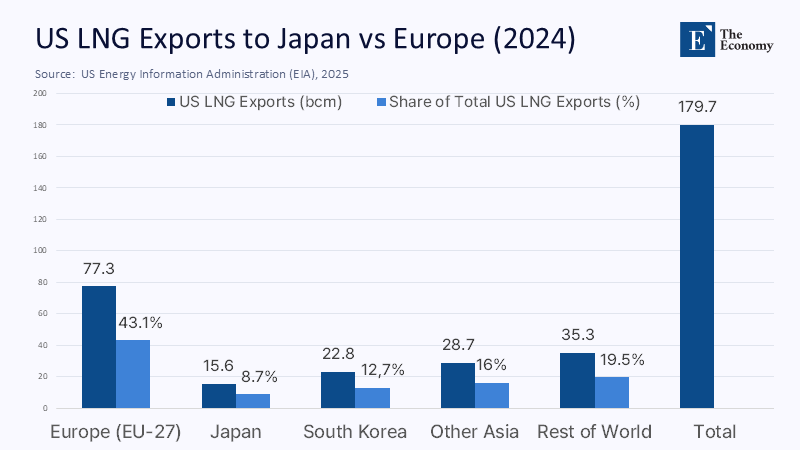

Energy security offers a crisp case study. Japan imported ¥542.6 billion (approximately US $3.8 billion) worth of US LNG in 2024, equivalent to only 8.7% of its total LNG bill—a share dwarfed by Australian cargoes and even by Russian volumes exempt from the G7 price caps. Freight economics explain why: shipping LNG from the US Gulf Coast adds roughly $2.50 per million BTU in transport costs, and from Alaska, the figure rises to $3.10 unless the State of Alaska shoulders the pipeline tariffs. Japanese utilities, therefore, treat Trump's LNG push as a price-discovery mechanism rather than a purchase order: JERA's June 2025 non-binding heads-of-agreement for up to 5.5 million tonnes a year merely reserves optionality post-2030.

Europe's offer is simultaneously subtler and more attractive. Under the EU–Japan Energy Transition Initiative launched alongside the sixth High-Level Economic Dialogue (HLED) in May 2025, Brussels opened joint procurement windows for green hydrogen certificates and guaranteed grid access for Japanese electrolyzers in Spain and Portugal—an arrangement that treats decarbonization not as charity but as co-insurance against supply disruption. In effect, Tokyo is trading a lumpy, politically contingent US gas deal for a modular, contract-law-based European diversification play.

Critical Minerals: When the Quiet Revolution Went Trans-Eurasian

If LNG is the headline, critical minerals are the footnotes that quietly decide industrial futures. The July 2023 Administrative Arrangement between the European Commission and the Japan Organisation for Metals and Energy Security (JOGMEC) formalized joint stockpile audits, environmental, social, and governance (ESG) benchmarks, and co-financing for greenfield extraction projects in Namibia, Chile, and Canada. That deal matters because Japan still sources over 60% of its rare-earth imports from China, while the EU depends on external suppliers for 98% of its lithium. By sharing risk-capital commitments and environmental due diligence teams, Brussels and Tokyo are constructing an insurance mechanism against either Chinese embargoes or US export-control whiplash. The EEU's Anti-Coercion Instrument, which has been in force since December 2023, provides an enforcement backstop. If Beijing or Washington penalizes the other's trade in strategic minerals, the latter can coordinate retaliatory tariffs within thirty days. Energy may dominate headlines, but gallium quotas and germanium permits are what keep semiconductor fabs running; Europe and Japan now jointly manage those chokepoints.

The Defence-Industrial Turn: GCAP, RAA and the End of Monopolies

Security cooperation is shifting from dependence on arms imports to co-development parity. The Global Combat Air Programme (GCAP), lodged in an international treaty ratified by the UK, Italy, and Japan in December 2023, allocates roughly US $27 billion in research and development through 2035; TTokyo'sshare—just over US $10 billion—already exceeds cumulative outlays on US Foreign Military Sales for the same horizon. Equally significant is the Reciprocal Access Agreement (RAA) with the United Kingdom, the first such pact Japan has signed with a European military power since 1902. It provides visiting forces status, streamlines customs clearance for matériel, and clears the legal ground for joint exercises in the Indo-Pacific and the North Atlantic. Add to that the co-production of radar modules with Thales in Brest and Japan's quiet participation in the EU's Permanent Structured Cooperation (PESCO) project on counter-hybrid warfare, and the pattern is unmistakable: Japan is distributing defense risk across multiple democratic supply chains, depriving Washington of its once near-monopolistic industrial leverage.

Digital Sovereignty and Subsea Cables: The Invisible Front

Tokyo's newest defense of autonomy lies in digital plumbing. The EU–Japan Digital Partnership, whose first Council meeting took place in July 2023, commits both sides to interoperable electronic identification frameworks and to "data Free Flow with Trust," a phrase that now appears verbatim in annexes to the EPA. Brussels adds muscle through the Global Gateway fund, which co-finances new Pacific subsea cables as redundant routes for data currently funneled through chokepoints near Taiwan and the Malacca Strait. Japan, for its part, is using overseas development assistance to splice a redundant spur into the Chuuk State cable in Micronesia, thereby protecting a corridor that carries traffic between Okinawa and the US mainland. The strategic logic echoes the raw-materials play: joint ownership of critical infrastructure raises the cost of coercion by any single actor, friend or foe.

Domestic Political Economy: Why the Kantei Quietly Cheers Diversification

Inside Japan, diversification garners rare bipartisan assent. Conservative security hawks welcome European technology transfers in areas where the United States still restricts them; progressive factions value Brussels ' ESG and data-protection templates as guardrails against American deregulation. Corporate chieftains in Keidanren read the EEPA's rule-of-origin liberalizations as a competitive lever against Chinese supply chains. At the same time, labor unions see higher value-added exports and, thus, more wage bargaining power. Even the Ministry of Finance, historically wary of foreign exchange risk, has begun issuing euro-denominated green bonds to finance hydrogen projects in Galicia and Apulia—evidence that the diversification thesis has colonized fiscal policy. Trumpian uncertainty, far from fracturing the policy consensus, has strengthened it: politicians can justify European hedges as prudent reactions to an unpredictable ally rather than as ideological experiments.

Policy Futures: Optionality as Deterrence

The emerging doctrine has four planks. First, hold the US nuclear umbrella, but surround it with a ring-fence of European and Indo-Pacific partnerships so that any American squeeze creates less leverage than before. Second, convert supply chains into networks rather than pipelines; redundancy, not efficiency, becomes the yardstick of national power. Third, institutionalize regulatory defense: the Anti-Coercion Instrument in Brussels and Japan's Economic Security Promotion Act will operate as mutually reinforcing shields. Fourth, monetize joint liabilities—such as shared mineral stockpiles, common submarine-cable routes, and cross-licensed AI chips—so that any aggressor must contemplate simultaneous retaliation from multiple democracies. Optionality, a long-standing financial term, is now a national security doctrine.

Diversification as the New Deterrent

The post-war script once read that Japan's safety lay in singular fidelity to the United States. That chapter is ending, not in rupture but in recalibration. Europe offers Tokyo something Washington no longer reliably provides: political predictability, regulatory convergence, and a share of industrial authorship rather than client-state consumption. In choosing to pivot westward across Eurasia even as Chinese pressure mounts and US energy ultimatums grow louder, Japan signals that twenty-first-century security is less about who protects you and more about how many partners you can turn to when protection frays. An alliance anchored in optionality is neither anti-American nor Eurocentric; it is post-Atlantic. The rest of the Indo-Pacific, watching a once risk-averse nation re-engineer its dependencies, will recognize the logic. In a world of weaponized interdependence, diversification serves as a form of deterrence.

The original article was authored by Silvia Menegazzi, a Junior Assistant Professor at the Department of Political Science, Luiss Guido Carli, and Head of Unit for the Asia Observatory. The English version, titled "Japan’s economic security strategy looks beyond the United States," was published by East Asia Forum.

References

European Commission. (2023). EU and Japan conclude landmark deal on cross-border data flows.

European Commission. (2024). EU–Japan trade picture and EPA five-year review.

European Commission. (2025). EU and Japan reaffirm cooperation at the 6th High-Level Economic Dialogue.

European Commission. (2023). Regulation 2023/2675 — Anti-Coercion Instrument.

Glenfarne. (2025). Strategic partner interest in Alaska LNG.

Japan Ministry of Defence. (2023). Record defence budget request for FY 2024.

Japan Ministry of Foreign Affairs. (2025). Outline of the 6th Japan-EU High-Level Economic Dialogue.

Japan Times. (2025). Japan imported ¥542.6 billion of US LNG in 2024.

JOGMEC & European Commission. (2023). Administrative Arrangement on Cooperation in Critical Raw Materials Supply Chains.

Ministry of Defence UK. (2023). Convention on the Establishment of the Global Combat Air Programme.

Prime MMinister'sOffice UK. (2023). UK–Japan Reciprocal Access Agreement.

Reuters. (2025, Feb 21). Trump seeks to reshape Asia's energy supplies with US gas.

Reuters. (2025, Jan 31). Japan weighs Alaska LNG pipeline pledge.

Reuters. (2025, Jun 11). JERA agrees to buy US LNG under 20-year contracts.

USTR. (2025). United States–Japan Trade Summary 2024.