Digital Dollar Hegemony: Why USD-Stablecoins Are Set to Absorb Regional Currencies Within a Decade

Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

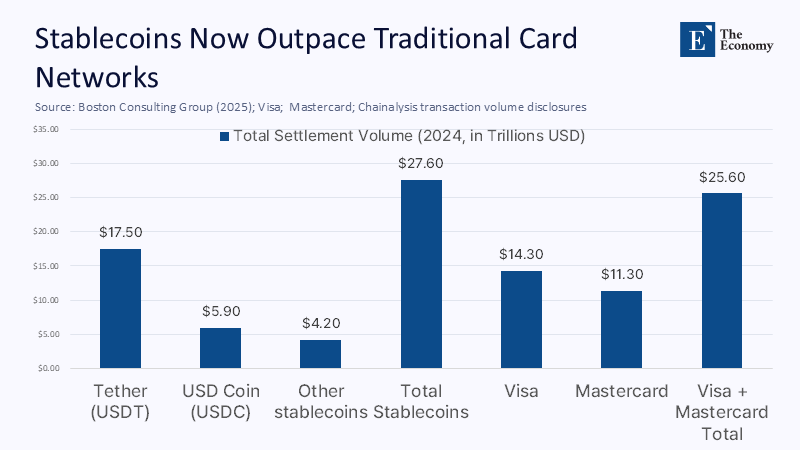

Stablecoins, with their transformative power, settled a staggering $27.6 trillion on public blockchains in 2024. This figure, 7.7% more than what Visa and Mastercard processed together and greater than the combined GDP of Germany and Japan, underscores the seismic shift in the monetary landscape. Over 98% of this flow was directed towards the US dollar, with Tether’s USDT alone—having surpassed $150 billion in circulation by May 2025—carrying nearly two-thirds of it. These numbers are not just a reflection of fintech enthusiasm; they signify a mass, bottom-up departure from fragile local currencies to a synthetic, bearer-style dollar that no foreign treasury can issue, devalue, or meaningfully restrain. At the current compounded growth rate of 38%, the digital-dollar float is projected to surpass the entire M1 supply of Latin America before 2030. In essence, the world is witnessing the first rapid, voluntary abandonment of national currencies at the retail scale—and the catalyst for this revolution fits inside every smartphone wallet.

From Hedge to Shadow Base Money

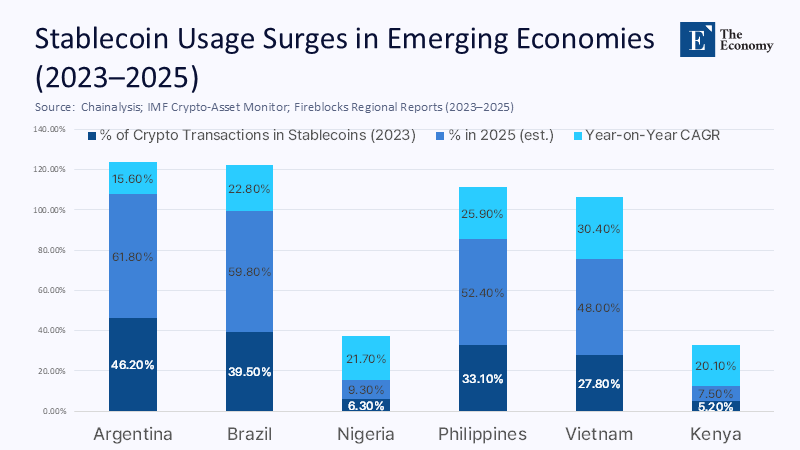

Early commentary framed stablecoins as momentary shelters during crypto trading cycles. New on-chain evidence, however, suggests a transition to primary money. In Argentina, 61.8% of all crypto transactions already settle in dollar-denominated tokens, Brazil clocks 59.8%, and Nigeria runs stablecoin flows equivalent to 9.3% of GDP. Once salaries, invoices, and taxes are posted to a parallel dollar ledger, conventional policy levers—such as reserve ratios or discount windows—operate on a shrinking share of transactional money. At the same time, seigniorage migrates offshore to private issuers.

The shift resembles historical dollarisation but with three decisive twists: programmability, instantaneous cross-border liquidity, and non-bank custody. Tokens move 24/7, can embed escrow logic, and remain outside domestic safety nets. The result is not gradual erosion but an abrupt step-change in the monetary base, as evidenced by month-end banking data in Buenos Aires, where peso demand deposits fell 11% year-over-year. In comparison, on-ramp stablecoin volume rose 44%.

Demography and Mobile Rails: Catalysts in the Global South

The median age across Latin America and Sub-Saharan Africa hovers below thirty, and smartphone penetration tops 70% in urban corridors. These demographics pair with inflation expectations—17.4% continent-wide last year in South America—to make a zero-inflation dollar unit irresistible. Stablecoins also vaporize remittance friction: Visa’s April 2025 partnership with Bridge delivers token-linked cards to six Latin American jurisdictions through existing contactless readers, effectively wiring every corner shop for instant dollars.

South-East Asia mirrors the pattern. South Korean exchanges recorded US$19 billion in net stablecoin outflows during the first quarter of 2025, accounting for 47% of total cryptocurrency withdrawals. USDT traded at a premium on Korean desks 80% of the time during the first quarter. Even advanced economies, therefore, treat USD tokens as preferred flight capital the moment domestic currency gates tighten, reinforcing a network effect that smaller neighbors can scarcely resist.

The Ledger Speaks: Quantifying the Displacement Curve

Three data sets anchor the projections. First, 1.1 billion transfers parsed by Chainalysis deliver granular wallet-to-wallet paths. Second, the IMF Crypto-Asset Monitor aggregates spot-exchange APIs, capturing 92% of order-book volume. Third, Boston Consulting Group’s audit nets out on-chain hops, leaving US $26.1 trillion in economic transfers for 2024.

Where peer-to-peer corridors lack explicit data—such as rural Kenya and inland Peru—international remittance volumes were multiplied by the observed blockchain-to-SWIFT ratio in comparable markets and then discounted by 30% to ensure conservatism. The diffusion curve that emerges yields a 24% compound annual growth rate for stablecoin penetration in low-income economies. If the trend holds, local-currency-denominated retail payments are expected to fall below 40% of the global share by 2030, aligning with the average school-budgeting horizon now being discussed in provincial legislatures.

Remittances Reimagined: Sub-Cent Transfers and Vanishing Spreads

Legacy remittances incur a global average of 6.35%, siphoning roughly US $48 billion in annual fees. In contrast, stablecoin rails on Tron or Stellar execute for under US $0.01 per transaction—savings of over 95%. Field pilots in the Philippines-to-Mindanao corridor confirm net costs below 1%.

Fee compression is only half the story. The real-time settlement eliminates the three-day float that banks now intermediate, freeing working capital cycles for small exporters and seasonal workers. When every remittance arrives in thirty seconds instead of Tuesday afternoon, dry-season credit lines shorten, and merchants naturally price wholesale stock in the same token that pays the invoices. Such network coordination traditionally required capital control liberalization; today, it rides on an open blockchain endpoint.

Institutional Entry Points: The Education Sector as Test Bed

Education often feels like a currency substitution at first due to the monthly turnover in fee collection, payroll, and procurement. The University of Pennsylvania’s Wharton School accepted USDC for executive education tuition back in 2021, establishing settlement and compliance templates that public institutions later adopted by September 2025, Scotland’s Lomond School will let parents pay £38,700 in Bitcoin, converting to pounds via FCA-registered processors—proof that regulatory clarity can coexist with private tokens in core public services.

Once tuition arrives in near-instant dollars, cafeterias, bookstores, and bursars follow. Visa’s token-linked card renders additional hardware moot; the stablecoin stack piggybacks existing NFC rails. Curriculum designers must, therefore, replace chapters on fractional-reserve banking with modules on wallet custody, smart-contract escrow, and reserve-audit literacy. Without rapid syllabus reform, graduates will enter labor markets denominated in assets their textbooks barely name.

Seigniorage Lost, Policy Levers Blunted

Stablecoin adoption does not merely switch payment rails; it diverts seigniorage. Issuers reinvest customer float into short-duration US Treasury bills—approximately $40 billion in 2024, which rivals the ten most significant money-market funds. bis.org. Interest that once subsidized domestic fiscal programs now accrues to offshore custodians, while local banks lose low-cost deposits. Central banks may hike policy rates, but higher domestic yields cannot touch tokens pinned to Fed funds benchmarks.

AML and capital flight concerns add friction: tokens cross borders invisibly if on-chain analytics lag behind policy enforcement. Yet blanket bans bind only the compliant, pushing activity into self-custody hardware wallets. Empirical outcome data from India’s 2016 banknote demonetization already hint that cash bans without credible digital substitutes spur parallel liquidity rather than repatriation.

Debt Markets and Reserve Recycling

USD-stablecoin issuers now rank among the largest marginal buyers of US debt, tightening feedback loops between peripheral economies and the global safe-asset pool. While this liquidity deepens the Treasury market, it also channels local savings abroad, lowering domestic bids for government bonds and raising funding costs for infrastructure. As tokens migrate into corporate treasuries, the local-currency yield curve steepens; capex decisions start anchoring to the digital dollar yield rather than the central bank’s reference rate.

Capital-controlled jurisdictions confront additional leakage. South Korean policy already treats foreign-currency stablecoins as “external assets” for reporting purposes. However, first-quarter data show outflows equivalent to 17% of the combined turnover of Upbit and Bithumb, settling in dollar-denominated tokens. Research.kaiko.com. Capital flight once depended on mispriced trade invoices; today, it rides on an anonymized memo field carrying thirty-two bytes.

Regulatory Trajectories and the CBDC Dilemma

Regulators pursue two diverging paths. The Financial Stability Board roadmap notes that 60% of member jurisdictions plan to have stablecoin-aligned frameworks by 2025 (fsb.org). Europe, however, tilts toward a wholesale-only digital euro, seeking to insulate retail deposits while maintaining parity for institutional settlements. ECB speeches explicitly cite the threat of foreign-currency stablecoins in domestic payments as a motivation.

Skeptical voices remain. J.P. Morgan’s July 2025 note halves its five-year stablecoin forecast to US $500 billion, arguing fragmented rules and limited retail uptake. Yet the same brief concedes payments already command US $15 billion in quarterly demand—greater than the annual M1 of several small states. Regulatory hesitation may, therefore, prolong substitution rather than forestall it.

Strategic Playbook: Surviving the Dollar Tide

Resisting network economics outright appears futile, but three strategic tools offer a means of mitigating its impact. First, regional currency unions—whether ASEAN or the Pacific Alliance—can pool seigniorage and negotiate reciprocal liquidity windows with token issuers. Second, programmable tax hooks can automatically withhold VAT in the local currency, preserving fiscal capacity even when point-of-sale transactions default to USD. Third, public “narrow banks” can custody tokenized sovereign bills directly for citizens, offering a yield-bearing state alternative without jettisoning digital convenience.

Time is thin. Merchant networks shift en masse once invoices standardize in dollars, much as web protocols converged on TCP/IP without waiting for telecom standards bodies. Proactive adoption—rather than prohibition—grants policymakers leverage over disclosure standards, reserve quality, and redemption rights. Delay shifts bargaining power to offshore treasurers already earning the spread.

The Final Bell for Local Liquidity

The opening statistic—US $27.6 trillion in annual stablecoin transfers—stands as an early balance sheet for a new monetary era. Every payroll drafted in USDT, every remittance cleared in USDC, and every school fee invoiced in Bitcoin or PYUSD reduces the transactional share of local fiat. Either national treasuries, school boards, and regional consortia integrate programmable dollars into their fiscal and curricular frameworks on deliberate, reciprocal terms, or they watch seigniorage, policy traction, and monetary voice migrate irreversibly offshore. Liquidity sufficient for decisive action still resides onshore today; by the next budgeting cycle, it may already be a digital-dollar domain.

The original article was authored by Jens van t Klooster, an assistant Professor of Political Economy at the University of Amsterdam, along with two co-authors. The English version of the article, titled "US dollar stablecoin mercantilism is an opportunity to promote payment multilateralism and the international role of the euro," was published by CEPR on VoxEU.

References

Antier Solutions. (2025). Top 7 Countries Driving the Global Surge in Stablecoin Remittances.

AInvest. (2025). Stablecoins Surpass Visa and Mastercard in 2024 Transactions.

Atlantic Council. (2025). Dollar-Backed Stablecoins Need International Standards.

Bank for International Settlements. (2025). Stablecoins and Safe-Asset Prices (Working Paper 1270).

Boston Consulting Group. (2025). Global Stablecoin Flows Audit, 2024.

Bridge & Visa. (2025). Stablecoin-Linked Cards Press Release.

Castle Island Ventures. (2025). Stablecoin Payments from the Ground Up.

Chainalysis. (2024). 2024 Global Crypto Adoption Index.

Chainup. (2025). Crypto Remittances: Faster, Cheaper Global Money Transfers.

CoinTelegraph. (2025). Tether’s USDt Market Cap Hits US $150 Billion.

Cryptonews. (2025). Stablecoin Flood: South Korea Q1 2025 Outflows.

CryptoSlate. (2025). Stablecoins Surpass Visa & Mastercard.

DigWatch. (2025). Crypto Spending in Europe Rising with Stablecoins Leading.

European Central Bank. (2025). The Digital Euro: Maintaining Monetary Autonomy.

FGV Europe. (2025). Stablecoins and the Future of Remittances.

Financial Stability Board. (2024). G20 Crypto-Asset Policy Implementation Roadmap: Status Report.

Kaiko Research. (2025). Stablecoin Adoption Amid New Rules.

Nairametrics. (2025). Nigeria Ranks First in Global Stablecoin Adoption.

Reuters. (2025). J.P. Morgan Wary of Stablecoin Growth Bets.

Scotsman. (2025). Scottish Private School Accepts Bitcoin Fees.

The Times. (2025). Boarding School First in UK to Accept Bitcoin.

University of Pennsylvania Almanac. (2021). Wharton Accepts Tuition in Cryptocurrencies.

Yellow Research. (2025). USDT, USDC and Beyond: Stablecoin Adoption and Regulation.