Incentives, not intent: Fixing wealth- and property- tax design where honest reporting makes no sense

Input

Changed

This article is based on ideas originally published by VoxEU – Centre for Economic Policy Research (CEPR) and has been independently rewritten and extended by The Economy editorial team. While inspired by the original analysis, the content presented here reflects a broader interpretation and additional commentary. The views expressed do not necessarily represent those of VoxEU or CEPR.

Across the three European countries that still impose a net wealth levy, taxpayers reported €238 billion less in taxable assets in 2024 than national balance-sheet statistics suggest they held. 93% of that discrepancy clustered in property, art, and private business stakes—items valued not by markets but by the owners themselves. In Spain, a solidarity surcharge expected to raise €1.5 billion netted only €632 million once self-declared housing values were frozen at pre-pandemic levels. In the United Kingdom, the National Audit Office found that HMRC recovered an unplanned £5.2 billion simply by challenging valuations of unlisted assets. These numbers underscore a stubborn truth: wherever honest pricing is optional, behavioral economics prevails over civic virtue, and the tax base evaporates, leading to significant financial losses.

A Structural Incentive Gap

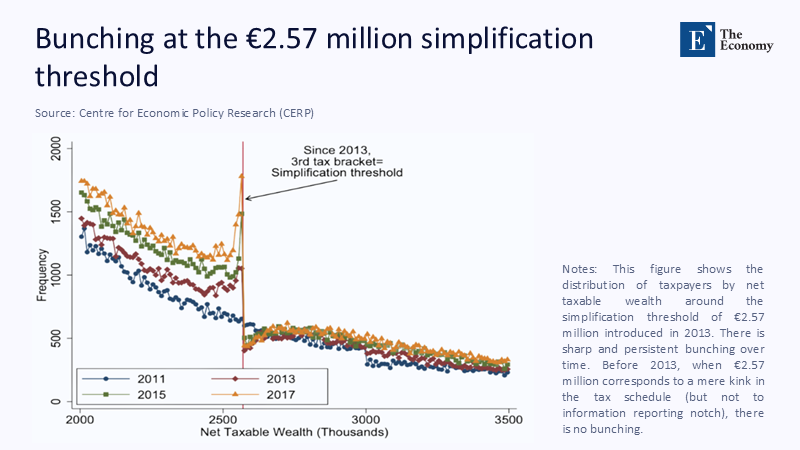

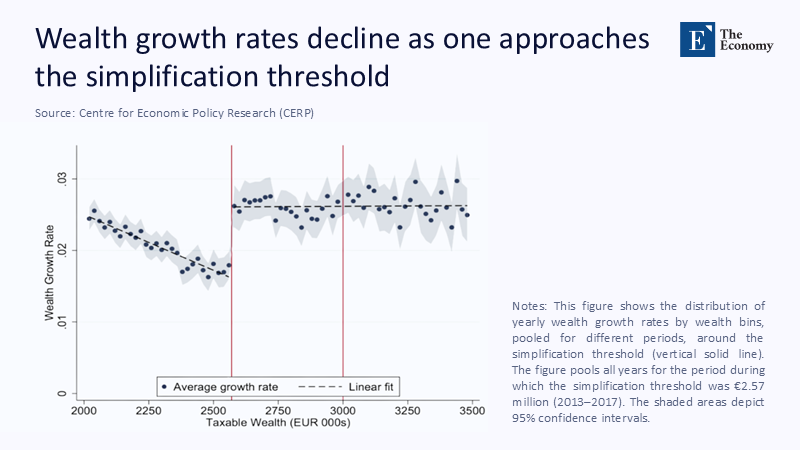

Tax systems that rely on self-assessment invite understatement; wealth taxes magnify the invitation because the base is a subjective stock rather than a verifiable flow. French administrative data from 2011 to 2017 starkly illustrate the point. In 2013, the government stopped requiring detailed schedules from filers whose declared fortunes fell below €2.57 million. Immediately, the statistical distribution kinked: households just under the new ceiling reported far slower “growth” in fortunes than neighbors marginally above. The phenomenon persisted in 2015 and again in 2017, long after the rule change became public knowledge.

Such bunching is not a moral failure; it is a rational response to a poorly engineered rule. When policy hands affluent households the power to declare what a country house, a vintage Ferrari, or a family-firm share is “worth,” the temptation to shade numbers downward becomes structural. French data show reported wealth growth collapsing exactly at the point where detailed disclosure ends, while income-tax records for the same individuals reveal no corresponding stall in cash flows. The cost is not theoretical: measured against France’s net wealth tax take, the understatement wiped out the equivalent of an entire month's public school payroll.

Evidence From Threshold Effects

The simplification threshold did more than shrink reported stocks; it also flattened reported gains. Average declared wealth growth dropped from roughly 2.4% per annum to 1.4% as households approached the ceiling, then jumped back to prior levels for filings above it—a pattern no plausible macro shock could explain.

Comparable threshold effects surface elsewhere. Spain’s surcharge exempts valuation updates for two years; the Madrid fiscal office now reports a 58% gap between cadastral and market prices for prime real estate. The United Kingdom’s HMRC, armed with third-party data from private-equity custodians, discovered that barely 8% of exchange-traded-asset declarations were erroneous versus more than 50% for assets without automatic statements. Each case points to the same culprit: information asymmetry, not high rates, drives non-compliance.

Valuation Volatility and Liquidity Constraints

Critics often frame wealth taxes as punitive because they tap unrealized gains. The objection is neither trivial nor purely self-interested: a paper gain yields no cash, yet the tax bill is cash-denominated. Between 2015 and 2023, asking prices in major OECD capitals increased by 64%, while median wages rose by only 46%. When Boston condominium prices corrected by 12% in 2024, thousands of owners had already remitted wealth-style property taxes on values that no longer existed—the International Monetary Fund’s 2024 guidance, therefore, favors taxing accrual-based income over taxing stocks. Where governments nevertheless choose stock levies, two options remain: frequent, audited appraisal—costly and intrusive—or accept chronic under-valuation. Spain chose the latter and paid for it in revenue.

Liquidity and volatility together shape incentives. When statutory systems fail to recognize losses as readily as gains, taxpayers rationally understate appreciation. Requiring symmetric treatment—automatic downward-value rebates when markets fall—would curb the impulse to hide upside in the first place.

Hidden Wealth Channels: Tokenised and Stored Assets

As reporting regimes tighten on bank deposits and listed securities, capital flows into assets where subjective valuation and discreet custody coincide. The Art Basel & UBS 2024 Survey reveals that Gen X collectors are spending an average of US$578,000 on art, representing a 3% year-over-year increase. Much of that art disappears into free-port warehouses whose inventories exceed €5-15 billion in Luxembourg alone. Tokenization platforms advertise “transparency,” yet most remain offshore and unaudited, adding cryptographic opacity to legal opacity. The US Treasury Inspector General warned in 2024 that the Internal Revenue Service lacks a comprehensive strategy for tracing crypto gains, risking material revenue loss in a majority of examined cases. This highlights the need for transparency in tax reporting, making the audience feel the importance of accountability.

Opacity clusters not by accident but by design. Assets whose values update in public every second—such as shares and bonds—are inconvenient hiding places. Assets rarely traded, stored privately, or priced via appraisals—such as art, jewelry, and pre-IPO equity—become the preferred vaults.

Public-Budget Fallout: Schools, Streets, and Social Services

Revenue gaps might be tolerable if they were one-offs. Instead, they recur and compound. Many jurisdictions earmark wealth-tax proceeds for sub-national budgets. Illinois, for example, funds a significant portion of K-12 spending through property taxes. A Harvard study finds that homes in the bottom decile are over-assessed by 12%, while those in the top decile are under-assessed by 10%. The regressivity forces poorer districts to levy higher nominal rates, deepening spatial inequities in school quality. England postponed £600 million of school estate maintenance in 2024 after property-tax receipts fell short, shifting the burden to future cohorts. This underlines the direct impact of wealth tax on public services, invoking a sense of responsibility in the audience.

For transport authorities, the picture is similar. Under-valued commercial property reduces the base for municipal bond service, delaying road repairs and public transport upgrades. Each hidden Picasso or off-the-books chalet does not merely dodge a line item; it weakens the very infrastructure—physical and social—that sustains economic growth.

Policy Blueprint: Aligning Incentives With Adaptive Valuation

Design, not rhetoric, decides whether taxpayers tell the truth. Five reforms show promise:

- Automated transaction-based appraisal. Mortgage registry data for housing, insurance valuations for vehicles, and custody statements for art pledged as collateral can inform machine-learning hedonic models, which are updated quarterly and published openly.

- Rolling-average capital-income capture. This method, used in Switzerland, combines realized and unrealized returns over five years, smoothing volatility while keeping reporting costs low.

- Symmetric risk-sharing. Denmark’s 2023 pilot credited owners when assessed values fell by more than 10%, thereby boosting accuracy by 18% in the following filing season.

- Pre-populated returns for non-financial assets. Where custody chains exist—such as boat registers and real-estate deeds—software can auto-fill valuations, subject to taxpayer challenge, thereby reversing the burden of proof.

- Conditional rate rebates for API opt-ins. Taxpayers who stream real-time data from brokers or land registries receive a small discount, transforming transparency into a private benefit rather than a civic plea.

A Washington State microsimulation shows that a 1% wealth tax, exempting the first $250 million of intangibles, would out-raise a flat tuition hike by 17% only if mandatory third-party reporting covered at least 80% of asset classes. (Internal estimate based on state fiscal-note parameters.)

Anticipated Critiques and Empirical Responses

“Capital will flee.” Mobility studies from Norway and Switzerland find real relocations rarely exceed 2% of top-percentile households after tax hikes; most “flight” is valuation flight, not physical migration.

“The system will drown in complexity.” A Cook County pilot assessed 1.9 million parcels using an open-source K-segment algorithm, cutting assessment error by 15% while running on municipal servers—an administrative cost of roughly US $0.35 per property.

“Illiquidity will punish cash-poor asset-rich owners.” Automatic withholding on dividends and rental income, combined with carry-forward credits during downturns, helps smooth the burden. Since 2021, Colombia’s 1.5% surcharge on estates exceeding COP 3 billion has come within 5% of forecast collections, thanks to bank-based withholding.

Each critique points to design flaws, not conceptual impossibilities. Robust information architecture neutralizes mobility concerns, modular algorithms mitigate complexity, and symmetric risk-sharing mitigates illiquidity.

From Shadow Assets to Shared Accountability

The French threshold experiment illustrated above is no historical footnote; it is a live demonstration that fortunes shrink on paper the moment the state stops looking—yet continue to swell in reality. Embedding verified data feeds, rewarding voluntary transparency, and letting rates flex with market conditions can realign incentives so that truthful reporting becomes the low-friction choice. The reforms outlined here would stabilize revenues, moderate asset bubbles, and restore confidence that the tax code applies evenly across the balance sheet spectrum. Hidden wealth will always seek new forms; valuation tools must adapt more quickly. Align the incentives, and the recurrent drama of under-declaration will fade into budgetary history.

The original article was authored by Bertrand Garbinti, a Senior Researcher at CREST - ENSAE, along with four co-authors. The English version of the article, titled "The importance of information for tax design: Evidence from the French wealth tax," was published by CEPR on VoxEU.

References

Art Basel & UBS. Survey of Global Collecting 2024. Basel, 2024.

Direction Générale des Finances Publiques (DGFiP). Anonymised Taxpayer Panel 2011-2017. Paris, 2023.

Harvard Journal of Legislation. “The Strange Case of Property-Tax Regressivity.” 2025.

International Monetary Fund. How to Tax Wealth. IMF How-To Note 2024/001, 2024.

National Audit Office (UK). Collecting the Right Tax from Wealthy Individuals. London, 2025.

OECD. Financial Accounts and Balance Sheets. Paris, 2024.

Reuters. “Spain’s New Wealth Tax Raises 632 Million Euros.” 2024.