"실리콘밸리 자금 몰린다" 새로운 대안으로 떠오른 해상 데이터센터, 상용화 장벽은 여전히 높아

"실리콘밸리 자금 몰린다" 새로운 대안으로 떠오른 해상 데이터센터, 상용화 장벽은 여전히 높아

입력

수정

판탈라사, 시리즈 B 라운드에서 1억4,000만 달러 조달 AI 시대 대안으로 떠오른 FDC, 자체 에너지 조달·냉각에 용이 통신 속도·유지보수 등 기술적 한계 뚜렷, 제도적 혼란도 예상

해상 AI 데이터센터 스타트업 '판탈라사(Panthalassa)'가 대규모 투자금 유치에 성공했다. 부지·전력 확보, 냉각 비용 등 기존 지상 인공지능(AI) 데이터센터의 한계가 속속 부각되는 가운데, 대안으로 플로팅 데이터센터(FDC)를 비롯한 해상 연산 시설이 주목받기 시작한 것이다. 다만 시장에서는 아직까지 기술·제도적 한계가 뚜렷한 만큼, 관련 개념이 상용화되는 데에는 상당한 시간이 걸릴 것이라는 전망이 지배적이다.

판탈라사, 데이터센터 시장 '다크호스'로

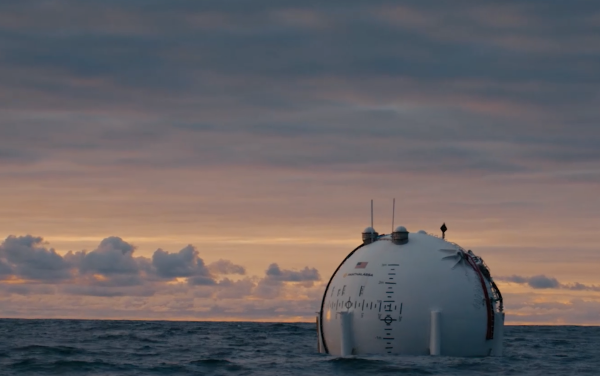

6일(현지시각) 파이낸셜타임스(FT)의 보도에 따르면, 최근 판탈라사는 페이팔 및 팰런티어의 공동 창업자 피터 틸이 주도한 시리즈 B 라운드에서 1억4,000만 달러(약 1,900억원)를 조달했다. 이로써 누적 투자 유치 금액은 2억1,000만 달러(약 3,040억원)로 늘었다. 오리건주 포틀랜드에 본사를 둔 판탈라사는 해양 파력을 이용해 전력을 생산하고, 이를 AI 연산에 직접 활용하는 오프그리드(off-grid)형 인프라를 개발 중인 기업이다. 사실상 바다 위에 떠 있는 AI 데이터센터를 구축하는 셈이다.

이러한 구상은 판탈라사의 자체 AI 컴퓨팅 노드 기술을 기반으로 한다. 먼 바다에 띄운 노드는 파도의 움직임으로 물을 끌어 올리고, 이를 가압 저장 후 방출해 터빈을 구동하는 방식으로 전력을 생산한다. 이 전력은 노드 내부에 탑재된 AI 칩을 구동하는데 즉시 쓰인다. 자체 발전을 통해 기존 지상 데이터센터의 막대한 전력 소모 문제를 해결한 것이다. 이에 더해 주변 바닷물은 무료 과냉각(Supercooling) 시설 역할을 수행하게 된다. 냉각 비용을 획기적으로 줄이면서도 연산 효율을 극대화할 수 있는 구조다. 데이터 송수신은 저궤도 위성(LEO)을 통해 이뤄진다.

판탈라사는 이미 2021년과 2024년에 오션-1과 오션-2 프로토타입 배치를 통해 기술력을 검증한 상태로, 이번에 확보한 자금은 포틀랜드 인근의 시범 제조 시설 완공 및 올해 중 북태평양에 배치될 예정인 오션-3 시리즈 노드 제작에 투입된다. 판탈라사는 오는 2027년을 상업적 배포 목표 시기로 설정했으며, 장기적으로는 수천 개에 달하는 노드를 해상에 띄우겠다는 방침이다.

해상 데이터센터 구축 시도 이어져

최근 시장에서는 판탈라사의 해상 인프라 개발과 유사한 시도가 속속 관찰되는 중이다. 지난해 10월 삼성물산과 삼성중공업이 오픈AI와 FDC 개발에 나서기로 협의한 것이 대표적인 예다. FDC는 바지선·선박·해양 플랫폼 위에 서버와 냉각 설비를 탑재하는 구조로, 판탈라사의 노드와 마찬가지로 지상 데이터센터 대비 부지 확보 부담이 적고 해수를 활용해 냉각 효율을 높일 수 있다는 장점이 존재한다. 다만 현시점 해당 사업은 별다른 진척 사항이 공개되지 않은 채 개념 검토 및 초기 협의 단계에 머무르고 있다고 전해진다.

오픈AI와의 사업 구상은 표류 중이지만, 삼성중공업의 관련 시장 진출 노력 자체는 여전히 이어지고 있다. 삼성중공업은 최근 미국 워싱턴DC에서 열린 ‘데이터센터월드(DCW) 2026’에서 미국선급(ABS)과 영국 로이드선급(LR)으로부터 자체 개발한 50메가와트(MW)급 FDC 모델의 개념설계 승인(AiP)을 획득했다. 글로벌 기준에 부합하는 기술 신뢰성을 확보한 셈이다. 이밖에 HD현대 계열사들도 관련 시장 진입에 속도를 내고 있다. HD현대중공업은 최근 미국 에이기리온에너지그룹(AEG)과 AI 데이터센터용 발전 설비 공급 계약을 체결했다. 선박 엔진 기반 발전 시스템을 데이터센터의 전력원으로 활용하는 방식이다. HD현대마린솔루션 역시 디지털·AI 기반 해양 인프라 사업 확대 가능성을 검토 중이다.

마이크로소프트(MS)가 2010년대 추진한 나틱 프로젝트 역시 유사한 전례로 꼽힌다. 나틱은 해저에 밀폐형 데이터센터를 설치하는 실험 프로젝트로, 담수로 구성된 열교환기가 밀봉된 서버에서 열을 흡수하고 외부 열교환기가 바닷물로 이를 식히는 구조가 적용됐다. MS는 2015년 미국 캘리포니아 해안에서 첫 시험 설비를 운영한 데 이어, 2018년에는 스코틀랜드 오크니 제도 인근 해저에 864대 서버와 27.6페타바이트(PB) 저장장치를 탑재한 데이터센터를 설치했다. 2020년 회수된 해당 서버들은 지상 데이터센터의 서버에 비해 1/8에 불과한 고장률을 보였다. 이 프로젝트는 FDC 개념의 초기 실증 사례로 평가된다.

단기간 내 상용화 가능성은 낮아

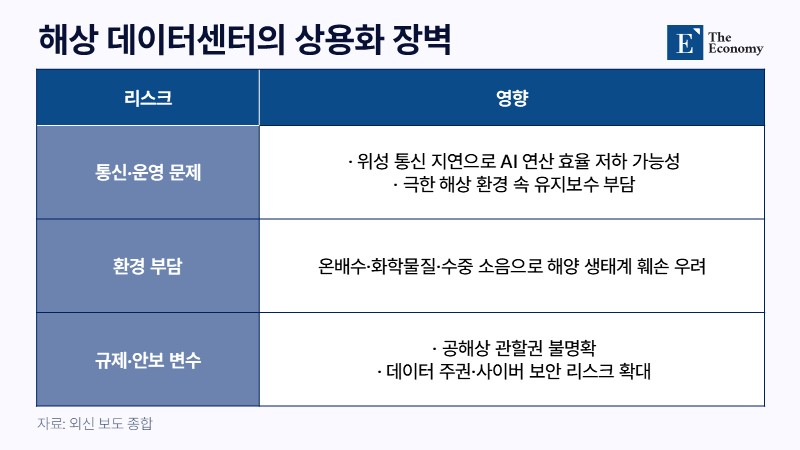

다만 업계에서는 이러한 해상 데이터센터 개념이 본격적으로 상용화되기 위해서는 아직까지 넘어야 할 벽이 높다고 지적한다. 가장 큰 걸림돌로 꼽히는 요소는 통신 속도와 대역폭이다. 광케이블로 연결된 지상 데이터센터와 달리 FDC는 위성 통신에 의존해야 한다. 대규모언어모델(LLM)을 구동하려면 수많은 노드가 유기적으로 협력해야 하는데, 이 과정에서 위성 통신 특유의 지연 시간은 연산 효율을 저해하는 요인으로 작용할 수 있다. 해상 환경의 특성 역시 난제다. 부식성이 강한 염분, 태풍 등 극한의 환경 조건을 견디며 고가의 AI 칩을 보호하는 데에는 상당한 유지보수 기술력이 필요하기 때문이다.

해양 생태계 훼손 가능성도 문제로 지목된다. 대규모 해상 데이터센터가 장기간 운영될 경우, 냉각 과정에서 발생하는 온배수가 주변 수온을 변화시켜 해양 생물의 서식 환경에 영향을 미칠 위험이 있다. 이에 더해 발전 설비와 배터리 시스템에서 발생할 수 있는 화학 물질, 수중 소음 문제 역시 해양 생태계에 부담으로 작용할 가능성이 크다. 실제 FDC와 유사한 환경 문제를 낳는 해양 플랜트 사업의 경우 규제와 지역 어업권 갈등에 부딪혀 프로젝트가 지연되거나 무산된 사례도 적지 않다.

국가 간 관할권 및 안보 문제도 해결해야 할 과제다. 공해상에 설치되는 FDC는 어느 국가의 법과 규제를 적용받을지 불분명한 경우가 많고, 데이터 주권 문제 역시 민감한 쟁점으로 떠오를 수 있다. 특히 AI 연산에 활용되는 대규모 데이터가 국경 밖 해역에서 처리될 경우 정보 보안과 사이버 공격 대응 체계에도 새로운 리스크가 생긴다. 결국 해상 데이터센터가 단순한 기술 실험을 넘어 실제 인프라로 자리 잡기 위해서는 단순 기술력 제고를 넘어 환경·규제·안보 전반에 걸친 국제 기준이 선제적으로 마련돼야 하는 셈이다.